Product & Technology

From Inspection to Impact

Data, video and artificial intelligence are driving service performance today, when inspection performance is closely tied to key business outcomes.

In Trump’s first year, just 60,917 pages were printed in the Federal Register, the official journal of the federal government, down 42%.

In the lighter federal regulatory environment of the Trump administration, government agencies employing prosecutorial discretion may often enforce dealer laws.

Pexels/Pixabay

In writing this article, I recall physicist Niels Bohr’s famous quip: "Prediction is very difficult, especially about the future.” I will endeavor to provide a very broad-brushed canvas of the coming year with some trepidation.

It’s essential for dealers to acknowledge that their current legal duties remain daunting. The many laws enforced by government and private plaintiffs will continue to challenge dealers, but who enforces the law is the question. The answer may be government agencies employing prosecutorial discretion.

Since the Reagan administration, there hasn’t been a starker contrast in enforcement approaches between federal and state regulators. This also applies to enacting new legislation. However, no government official can totally abandon his or her duties, which an oath was taken to enforce, so all present dealer legal obligations need to be discharged.

“Tone at the top” was originally an accounting term, but is now often used to describe the general corporate culture established by an organization's leadership. In this case, it is the Trump administration, which abhors government regulation.

The Federal Register is the official journal of the federal government of the United States and contains government agency rules, proposed rules, and public notices. It is published daily and measures the degree of federal regulation based on the number of pages published at the end of the year.

In Biden’s last year, 2024, 106,109 pages were published, the highest number ever tallied. In Trump’s first year, 2025, only 60,917 pages were printed, a whopping 42% reduction in regulations in one year.

This tone at the top of the federal government resounds throughout many agencies. However, this tone at the top strikes a dissonant note in some state governments and consumer interest groups.

The new acting director of the CFPB, Russell Voight, is the antithesis of its former director, Rohit Chopra, a rabid consumer advocate. It would take an act of Congress to eliminate the CFPB, a goal announced by former Department of Government Efficiency director Elon Musk, but Voight approached this ambition by reducing the agency’s workforce by 88%, or 1,500 employees.

In addition, he is reducing its funding by limiting the Federal Reserve Board’s funding requests and repealing many of the CFPB’s regulations, such as fair lending and consumer complaint disclosure requirements.

A feared tool of the CFPB had been its auditing power, but this is now severely tempered, with a 50% reduction in these operations and forcing the examiners to read a “Humility Pledge.”

The FTC has also been revamped, with the current controlling commissioners showing a mindfulness toward business concerns through a conservative approach to regulation. It is also a provident prediction that rulemaking will be curtailed but not totally limited.

An important example of the shift in FTC policy is its announced decision to abandon disparate impact as a discrimination policy. However, it is important to note that Chairman Ferguson has voted in favor of various prosecutions of dealers in the past, including multimillion-dollar settlements with Arizona and Illinois dealership groups.

For both the CFPB and the FTC, novel theories of liability will become rare.

Two Supreme Court decisions are also germane. In "AMG Capital Management," the FTC was barred from seeking equitable monetary relief in its prosecutions. Congress will not reinstate this power under the present administration.

The court also overturned the "1984 Chevron" deference doctrine, which limits the authority of federal agencies: courts needn’t defer to agency opinions.

According to the annual Consumer Federation of America report, auto-related issues have been the top consumer complaint category for the past nine years. This includes new and used motor vehicle sales, leases, and auto repair shop issues.

Consumer complaints can’t simply be ignored by the government. These issues are addressed by legislation and prosecution. All states may act, but the "blue" states will be more activist.

In particular, members of DAGA, or the Democratic Attorneys General Association, have announced their willingness to advance consumer protection in the absence of federal action. The Dodd-Frank Act, which established the CFPB, provides state attorneys general the right to enforce its provisions, an enlargement of state authority. Regulators will attempt to utilize these formidable powers.

Consumer complaints can’t simply be ignored by government but are addressed by legislation and prosecution.

Pexels/Erik McIean

State legislators must propose legislation to justify their existence. In 2025, 132 vehicle finance bills were enacted from the 784 proposed. In 2026, bills relating to auto dealers will continue unabated.

Vehicle finance is an expansive category that addresses vehicle sales, including sales tax issues, dealer franchise issues, payment assurance devices, vehicle service contracts, liens, and debt collections and repossessions.

In the 2025 legislative cycle, the significant issues addressed included retail installment sale contracts, Guaranteed Asset Protection, titling and lien Issues, and collection and repossessions. Tangential issues were also considered, such as vehicle sharing, automated license plate recognition systems, and transportation network companies.

With the degradation of the CFPB, several states have taken this Trump policy as an incentive to enhance measures at the state level. Multistate attorney general actions have been initiated, with many attorneys general expressing concerns for the administration’s handling of the bureau. DAGA, in particular, will continue its legal challenges to the Trump administration.

The FTC has prosecuted dealers and settled for over $57 million in the past five years. During the same time frame, state agencies settled for over $47 million. These cases will continue. Consumer interest groups have begun mobilizing to demand action and have announced their intentions at their recent conferences.

For example, the National Consumer Law Center and Consumer Federation of America featured numerous speakers highlighting the need to fill the federal regulatory gap with lawsuits and regulatory actions during their fourth-quarter conferences.

Consumers can sue through private rights of action by hiring willing attorneys who specialize in suing dealers. Many federal and state laws include a private right of action, such as the Telephone Consumer Protection Act, California Consumer Privacy Act, Fair Credit Reporting Act, and the Equal Credit Opportunity Act.

And of course, the omnipresent Unfair or Deceptive Acts or Practices always provides opportunities to sue dealers, including mass and class actions.

Pexels/RDNE Stock Project

The Fifth Circuit Court of Appeals overturned the FTC’s Combating Auto Retail Scams, or CARS Rule, on procedural grounds. The FTC has not filed a petition for a writ of certiorari to appeal the decision and probably won’t do so.

Consequently, state versions of the CARS Rule, as was enacted in California, will be promulgated and will increase the regulatory burden on dealers.

As a corollary to the CARS Rule, many states are enacting laws to ban hidden "junk fees" and promote pricing transparency, requiring dealers to clearly disclose all costs and fees upfront. An example of these laws is Oregon's Auto Loan Fairness and Transparency Law, which standardizes vehicle transactions. Dealer documentary fees may also be characterized as junk fees pursuant to these new laws.

At least 20 states, including California, Florida and Texas, have enacted new data privacy and security laws. Several other states are considering similar legislation. These laws often give consumers rights over their personal data and impose obligations on businesses to safeguard that data.

A 2023 overhaul of the FTC Safeguards Rule included franchise dealers who must implement a substantial safeguards program. It will be a subject of investigation, as will as its companion rule, the FTC Privacy Rule. This collection of laws creates a labyrinth of compliance concerns.

The Office of Foreign Assets Control statute of limitations increased from five years to 10 years. Dealers need to review their protocols to effectuate this new law.

Auto lending fraud losses reached $9.2 billion in 2024 in response to criminal activity, such as synthetic identity fraud. Dealers will be responsible for enforcing the Red Flags Rule, among other fraud-prevention procedures.

Consumer-protection regulations and enforcement are increasingly focused on consistent pricing and proper disclosures for voluntary protection products and their refunds. Legislation and legal action are compelling possibilities.

Some states are re-examining their consumer-protection acts and contemplating various revisions. For example, New York State enacted the FAIR Business Practices Act, which expands the authority and application of UDAP in New York. States such as California, Illinois and Minnesota considered bills this past year that would grant increased authority to state regulators to enforce consumer laws.

Pennsylvania Democratic Gov. Josh Shapiro cited the CFPB cuts while launching a centralized consumer-protection hotline, website, and email address to make it easier for Pennsylvanians to report scams, resolve financial and insurance issues, and access help from the commonwealth in one place.

Many consumer-enforcement agencies are monitoring these developments, including the mini-CFPBs in certain states and municipal consumer agencies.

New vehicles must have the technology to passively detect if a driver is impaired by alcohol and prevent the vehicle from operating. Dealers will need to ensure the vehicles they sell comply with these new safety standards, which could be in place as soon as late 2026.

There is a cornucopia of other issues dealers should continue to monitor, such as OEM data sharing and the ubiquitous issue of artificial intelligence, which will affect all aspects of the industry.

Despite the new compliance direction on the federal level, these are the many issues dealers need to contemplate. The liability challenge is staggering. However, in reviewing this article, the reader may take solace in the observation of ancient Chinese sage Lao Tzu, who said, “Those who have knowledge don’t predict. Those who predict don’t have knowledge.” Please be kind in your opinion of the messenger.

Terry O’Loughlin is director of compliance for Reynolds and Reynolds and is admitted to the Pennsylvania and Florida bars. Before joining Reynolds, he was employed by the Florida Office of the Attorney General, where he investigated automobile dealers and financing sources. He previously was a public accountant.

Loading data...

Product & Technology

Data, video and artificial intelligence are driving service performance today, when inspection performance is closely tied to key business outcomes.

Awards

Buffeted by trial after trial as a young man, David Wright knew he’d found his life path when he stumbled into auto retail after all other doors slammed shut. The 2026 Time Dealer of the Year shares the lessons he learned along the way.

Industry

Understanding the risks and benefits of retail accounting and Super CFCs can help you better present options to your dealer partners.

Actuary

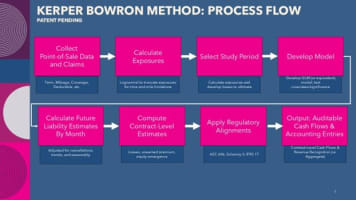

The Kerper Bowron Method is a patent-pending approach that builds on established actuarial principles but applies them at the individual contract level.

Industry

Providers and administrators should clearly and credibly communicate their experiences since their numbers will draw more scrutiny this year.

Compliance

In Trump’s first year, just 60,917 pages were printed in the Federal Register, the official journal of the federal government, down 42%.

Industry

As America turns 250, explore how the automotive industry shaped jobs, culture, innovation, and mobility from Detroit assembly lines to today’s EV era.