Product & Technology

From Inspection to Impact

Data, video and artificial intelligence are driving service performance today, when inspection performance is closely tied to key business outcomes.

The Kerper Bowron Method is a patent-pending approach that builds on established actuarial principles but applies them at the individual contract level.

Contract-level modeling delivers granular cash-flow projections reflecting actual service delivery patterns.

Kerper Bowron

*Summarized by AI

For decades, service contract accounting has operated on methods that were adequate for compliance but fundamentally imprecise.

The extended warranties, vehicle service contracts, and protection plans generating billions in annual revenue have been accounted for using aggregate approaches better suited to the 1990s than today’s data-driven environment. That era is ending.

The shift is already gaining traction: The Kerper–Bowron Method, detailed in a peer-reviewed paper published in Risks (MDPI, February 2026) represents the first practical implementation of contract-level precision in this space.

A new patent-pending methodology emerging from actuarial practice promises to transform how finance teams handle these contracts, moving from portfolio estimates to individual contract precision.

The implications extend far beyond technical compliance. This represents a complete rethinking of the management of service contracts, revolutionizing revenue recognition, product development, and capital efficiency and requirements.

Consider a typical scenario: A company sells 10,000 vehicle service contracts in a quarter. Under current practice, finance teams recognize revenue using earnings curves, or predetermined patterns estimating when services will be delivered over the contract term. These curves, while better than straight-line recognition, treat all contracts as essentially identical.

This imprecision has real costs. CFOs maintain larger reserve buffers than necessary because they lack confidence in liability estimates. Revenue recognition lags or exceeds actual performance patterns, creating timing mismatches. And perhaps most critically, the capital tied up in the reserve accounts — which can reach tens of millions of dollars for large programs — sits idle when it could be deployed more productively.

The service contract industry has long accepted this imprecision as a cost of doing business. It need not be.

The new method applies probability to each contract rather than to portfolios as a whole.

Pexels/PNW Production

The breakthrough comes from applying probabilistic modeling to individual contracts rather than portfolios.

By incorporating specific attributes — vehicle make and model, initial mileage, coverage terms, manufacturer warranty provisions, and expected driving patterns — you can now project month-by-month cash flows with remarkable precision.

This isn’t theoretical. Early implementations show projection errors below 3% over 12-month horizons for programs with sufficient volume, and often under 1% in stable conditions. The result is meaningful for every partner in the service contract ecosystem: retailers, dealers, agents, administrators and insurance companies.

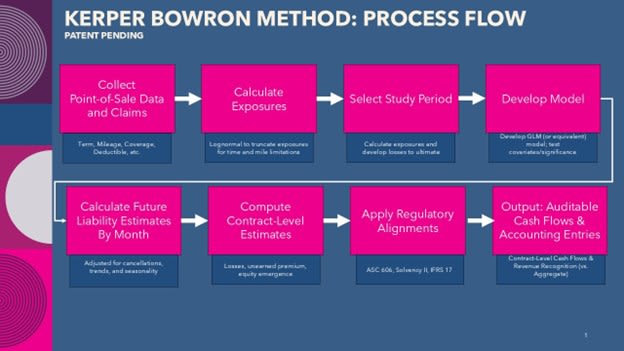

What emerged from this work is the Kerper Bowron Method, a patent-pending approach (US Provisional Patent Application No. 63/858,053) that uses only point-of-sale data to generate precise, month-by-month probabilistic cash-flow projections for every single contract. It replaces 40-year-old aggregate earnings curves and block reserving with an auditable, contract-specific formula.

The approach builds on established actuarial principles but applies them at the individual contract level.

A traditional actuarial analysis would occur at the administrator or carrier level. These general assumptions may not provide much accuracy at smaller segments, such as dealer, location or agent. By providing an individual contract estimate, allocations are much more efficient and accurate.

The timing couldn’t be better. Global accounting standards have evolved significantly, ASC 606 in the United States and IFRS 17 internationally both emphasizing claim- and cancel-based revenue recognition. Meanwhile, Solvency II in Europe demands probability-weighted cash flow projections for insurance-like contracts.

Contract-level modeling delivers precisely what these standards require: granular cash-flow projections reflecting actual service delivery patterns.

A finance team implementing this approach can simultaneously satisfy ASC 606’s performance obligation requirements, support IFRS 17’s fulfillment cash flows, and provide Solvency II’s probabilistic projections, all from a single analytical framework. The Kerper Bowron Method is in fact the first approach to mathematically satisfy the EU’s “ideal equation” (Article 77) for finite, predictable risks, something previously considered unsolvable for insurance exposures. Even direct manufacturer warranty liabilities can leverage this process for accruals or insurance transactions that derisk the balance sheet.

This convergence matters practically. Multinational organizations often maintain separate reserve methodologies for different regulatory regimes, creating reconciliation headaches and governance challenges.

Contract-level precision offers a unified approach that meets multiple requirements without the traditional trade-offs between accuracy and complexity.

Authors Kerper and Bowron

Kerper Bowron

Another compelling application extends beyond pure compliance. In the U.S. auto dealership industry, owners have long viewed their service contract reserve accounts as unavailable capital, legally theirs but functionally locked away until contracts mature and profits emerge naturally over time.

Contract-level projections change this calculus entirely. When you can project individual contract profitability with high confidence, you can support lending decisions against those projected cash flows. The reserve account transforms from a passive liability cushion into an active source of liquidity. In jurisdictions permitting it, the difference between projected losses and required reserves can be unlocked as instantly lendable, self-liquidating capital secured solely by the contracts themselves.

The process is straightforward:

A dealership principal who previously waited three to five years for service contract profits to emerge can now access that capital in months, redeploying it into inventory, facility improvements or other growth initiatives.

Industry modeling suggests the method’s improvements in actuarial precision, reserve management, and capital unlocking could yield efficiencies of $4 billion to $9 billion per year in the U.S. auto VSC market alone through reduced operational costs, minimized over-reserving, and unlocked lending capital across the sector.

The transition to contract-level accounting is not trivial, but the barriers are lower than many finance leaders assume. Core requirements are clean contract-level data (which most organizations already maintain), sufficient historical experience to build predictive models, and analytical capability to score contracts at the point of sale.

The modeling leverages standard statistical techniques, primarily Generalized Linear Models that insurance actuaries have used for decades. What’s new is applying these methods at the individual contract level and integrating output directly into financial reporting systems. The Kerper Bowron Method is already running full contract projections for one leading administrator, demonstrating that this isn’t incremental improvement but the first true contract-level accounting engine for the industry.

Organizations should expect a six- to 12-month implementation timeline, including model development, system integration, and control framework establishment. The investment is modest compared to major ERP initiatives, while the return, in reduced reserves, improved forecasting, and potential capital access, can be substantial.

Results can be tested during the development phase so that the variance of the projection can be established before implementation.

This shift toward contract-level precision signals the maturation of service contract financial management, moving from population-based estimates to individual-level predictions, much as customer analytics evolved in retail and banking. The method spans from electronics and appliances to heavy commercial equipment, making its applicability as broad as the service contract market itself.

For administrators and reinsurers, traditional earnings curves and periodic large-block analyses become obsolete. Real-time visibility into claims, cancellations and equity emergence enables proactive budgeting and risk management in ways that simply weren’t possible before.

The competitive implications are significant. Organizations adopting precision accounting methods will carry lower reserve buffers, produce more accurate forecasts, and potentially access capital previously trapped in reserve accounts. Those clinging to traditional methods will find themselves at a growing disadvantage, not because their accounting is wrong, but because it’s imprecise in ways that increasingly matter.

For finance leaders overseeing service contract portfolios, the question isn’t whether to adopt these methods but how quickly they can implement them. The technology exists, the regulatory framework supports it, and the business case is compelling.

Better accounting isn’t just about compliance. It's about competitive advantage. Finance leaders ready to explore contract-level precision should start with a data assessment and pilot projection. Contact us to discuss how this can fit your portfolio.

ABOUT THE AUTHORS: John Kerper and Lee Bowron are co-partners of the Kerper Bowron firm, which offers claims adjusting and actuarial services for finance-and-insurance, captive lenders and self-insured programs.

EDITOR’S NOTE: This article was authored and edited according to Providers & Administrators editorial standards and style. Opinions expressed may not reflect that of the publication.

Loading data...

Product & Technology

Data, video and artificial intelligence are driving service performance today, when inspection performance is closely tied to key business outcomes.

Awards

Buffeted by trial after trial as a young man, David Wright knew he’d found his life path when he stumbled into auto retail after all other doors slammed shut. The 2026 Time Dealer of the Year shares the lessons he learned along the way.

Industry

Understanding the risks and benefits of retail accounting and Super CFCs can help you better present options to your dealer partners.

Actuary

The Kerper Bowron Method is a patent-pending approach that builds on established actuarial principles but applies them at the individual contract level.

Industry

Providers and administrators should clearly and credibly communicate their experiences since their numbers will draw more scrutiny this year.

Compliance

In Trump’s first year, just 60,917 pages were printed in the Federal Register, the official journal of the federal government, down 42%.

Industry

As America turns 250, explore how the automotive industry shaped jobs, culture, innovation, and mobility from Detroit assembly lines to today’s EV era.