Product & Technology

From Inspection to Impact

Data, video and artificial intelligence are driving service performance today, when inspection performance is closely tied to key business outcomes.

Providers and administrators should clearly and credibly communicate their experiences since their numbers will draw more scrutiny this year.

Administrators who can clearly articulate and defend their performance drivers preserve valuation.

P&A Magazine

As the F&I and warranty administration sector settles into 2026, the mergers-and-acquisitions landscape looks markedly different from what it did at the height of post-pandemic consolidation.

Transaction activity no longer reflects the near-feral pace of 2021 and 2022, when capital was abundant, multiples expanded rapidly, and roll-up strategies dominated headlines. Today’s market is more measured but far from moribund.

The reset reflects broader economic dynamics, most notably in the underlying automotive market, which drives demand for finance-and-insurance products.

According to Cox Automotive’s 2026 outlook, new-vehicle sales are projected to moderate to approximately 15.8 million units, a slight decline from 2025 but still indicating solid, if not accelerating, demand.

Used vehicles and broader mobility trends are expected to remain key contributors to dealer economics in the year ahead. This backdrop of stability without rapid expansion is shaping how buyers and sellers think about value and risk.

Capital is still being deployed in the space, but the type of capital and the way transactions are structured have shifted meaningfully.

Administrators who can clearly articulate and defend their performance drivers preserve valuation.

P&A Magazine

One of the most significant developments in the sector is the active role of strategic insurance buyers. In October 2025, Protective Life Corp., a U.S. subsidiary of Dai-ichi Life Holdings, announced an agreement to acquire Portfolio Holding and its subsidiaries from Abry Partners.

This was not a sponsor-to-sponsor trade; it was long-term strategic insurance capital choosing to deepen its foothold in the F&I value chain. Similarly, Fortegra’s agreement to be acquired by DB Insurance reinforces the theme of international and strategic insurance-backed buyers pursuing platforms with underwriting discipline, product breadth, and scalable distribution.

These deals underscore what today’s acquirers are prioritizing: predictable underwriting income, robust reinsurance management, and distribution strength.

Strategic buyers are focused on functional depth rather than simple aggregate scale, signaling a maturation of capital allocation in the space.

The pace of independent F&I agency acquisitions has slowed. Between 2018 and 2022, private equity-backed platforms pursued aggressive buy-and-build strategies, often rewarding scale and add-on velocity with attractive valuations. That momentum has eased.

Higher cost of capital, integration challenges from earlier roll-ups, and heightened scrutiny of organic growth have made buyers more selective.

Independent agency transactions are still occurring, but today’s acquirers are evaluating factors that matter more for long-term durability: client diversification, producer dependency risk, concentrated revenue streams, and sustainable growth drivers rather than simply adding units to a platform.

In short, scale alone is no longer the sole determinant of value. Durability matters.

Valuation multiples in the F&I and administration space remain healthy when benchmarked against long-term norms, but they are anchored by fundamentals rather than exuberance.

One of the defining characteristics of recent deals is the use of structured consideration, particularly earnouts and performance-based components.

Buyers are increasingly allocating a significant portion of total consideration to future performance milestones. This reflects the inherent uncertainty that arises from forward earnings assumptions, reinsurance economics, shifting loss experience, and contract performance.

Rather than assigning aggressive headline multiples, buyers are explicitly pricing risk, using structure to bridge valuation gaps.

This approach benefits both sides when anchored in defensible metrics. Sellers achieve upside for outperformance, and buyers protect against downside volatility.

Cox Automotive expects a modest moderation in new-vehicle sales this year but an overall stable market.

Pexels/RDNE Stock Project

Across administrator transactions, loss ratio is consistently the central underwriting variable, and the accuracy of that metric depends largely on revenue recognition and earnings curve methodology.

Administrators who rely on overly simplistic revenue curves, such as pro-rata allocation, can unintentionally distort loss ratios when claim timing is uneven. In contrast, experience-based curves that align revenue with claim incidence can materially change normalized results, often revealing stronger long-term profitability than pro-rata figures suggest.

In 2026, buyers should continue to dig deeper into:

The quality of these analytics increasingly dictates deal outcomes. Administrators who can clearly articulate and defend their performance drivers preserve valuation; those who cannot risk erosion in diligence.

Looking ahead, several broad themes are likely to define the coming year:

The F&I ecosystem remains attractive. It is not a space for fleeting momentum but a space for measurable performance. The auto market may not be expanding at headline-grabbing rates, but it is steady. This year, M&A success will depend less on timing and more on preparation, clarity of performance metrics, and defensible underwriting.

Providers and administrators who understand their own experiences and who can articulate them credibly will find capital. The difference in 2026 will not be whether capital exists but whether your numbers withstand scrutiny.

Loading data...

Product & Technology

Data, video and artificial intelligence are driving service performance today, when inspection performance is closely tied to key business outcomes.

Awards

Buffeted by trial after trial as a young man, David Wright knew he’d found his life path when he stumbled into auto retail after all other doors slammed shut. The 2026 Time Dealer of the Year shares the lessons he learned along the way.

Industry

Understanding the risks and benefits of retail accounting and Super CFCs can help you better present options to your dealer partners.

Actuary

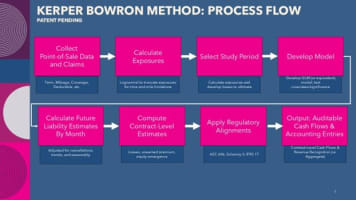

The Kerper Bowron Method is a patent-pending approach that builds on established actuarial principles but applies them at the individual contract level.

Industry

Providers and administrators should clearly and credibly communicate their experiences since their numbers will draw more scrutiny this year.

Compliance

In Trump’s first year, just 60,917 pages were printed in the Federal Register, the official journal of the federal government, down 42%.

Industry

As America turns 250, explore how the automotive industry shaped jobs, culture, innovation, and mobility from Detroit assembly lines to today’s EV era.