Words Matter: Use the Right Ones to Define Lenders

Words Matter: Use the Right Ones to Define Lenders

How often have you been in a conversation when the person is using one word, but means something else? It can be confusing and lead to miscommunication. Frequently we do this in the F&I industry without realizing how the words we use can create an inaccurate impression.

While we occasionally indulge in “alternative” definitions, our language choices can have significant implications for our industry and our individual companies when they are taken literally by regulators and courts. Bottom line: Words matter!

Take the word “lender,” for example. It’s used to describe a wide variety of financial entities, from state or national credit unions and banks to dealers acting as retail sellers providing financing. Sometimes people use lender to loosely mean “the original retail creditor and the entity that buys or takes assignment of the finance contract.” Those are a lot of options when trying to determine which type of lender someone is talking about.

In this brief article, we’ll journey into the jungle of lender definitions common in our industry, and I’ll do my best to avoid too much legalese and jargon. Let’s jump right in, shall we?

Dealers and Lenders

In the auto retail environment, a vehicle purchase is often originally financed by the dealership itself. In this instance, the dealership is not a licensed or chartered creditor, but offering the credit to the purchaser within the dealership’s capacity as a retail seller. The credit is extended to the customer as dealer-initiated financing, which is a retail installment sales contract (RISC). The dealer then sells or assigns the RISC to a different type of lender.

This new lender can be a bank, trust company, savings and loan association or credit union, or it could be structured as a sales finance company pursuant to state law. To the consumer purchasing the automobile and signing the RISC, this transaction is almost always transparent. Frequently the dealer already knows which entity will buy the RISC and that entity is often on all of the finance documents. To the consumer, the assigned lender looks as if it is the originating lender.

The overarching difference between the variety of lenders has very little to do with the financing transaction, but with the regulations and regulatory bodies that govern the various institutions. The good news for these entities is that they can choose their regulator when they establish their charters. For example, banks can be regulated either by the Office of the Comptroller of the Currency (OCC), the Federal Deposit Insurance Corporation (FDIC), and/or a state regulatory agency, depending on their charter. Credit unions are in the same boat, with the regulator determined by the structure the institution selects when forming.

Sales Finance Companies

Sales finance companies are permitted under state laws and therefore regulated at the state level. Credit unions have similar distinctions depending on their structure. But regardless of their regulator, a credit union must be non-profit, tax-exempt, and made up of “members” who use the financial services offered by the credit union.

Sales finance companies are another type of entity that can purchase loans originally sold as RISCs. They are defined by state law and frequently permit an otherwise nonfinancial institution to purchase RISCs.

Arizona’s definition of this type of lender is instructive and comparatively simple. It defines a sales finance company as “a person engaged, in whole or in part, in the business of purchasing retail installment contracts from one or more retail sellers.” The statute then goes on to provide a regulatory framework for the entities, without requiring a charter as would a bank, credit union, trust, or other institution.

While we all wait to see what happens with the CFPB’s authorities and structure, that agency understood very well the difference between these types of entities and found creative ways to assert its powers over even state-regulated lending institutions that loan money for vehicle purchases.

In 2015, it took jurisdiction for supervisory authority over large nonbank lending institutions. But this article is not about the CFPB’s perspective on lending institutions. That story would take up much of this publication.

Hopefully this short discussion provided you some context and a reminder about the proper use of terminology when discussing the lenders we work with.

More Industry

Tesla Tops American-Made List

As automakers have pulled back on EV production in the U.S., the number of vehicles on Cars.com’s American-Made Index has declined, though hybrids remain popular.

Read More →

Black, White and Gray

U.S. consumers have increasingly favored achromatic shades for their vehicles, though the trend seems to have plateaued, new research shows.

Read More →

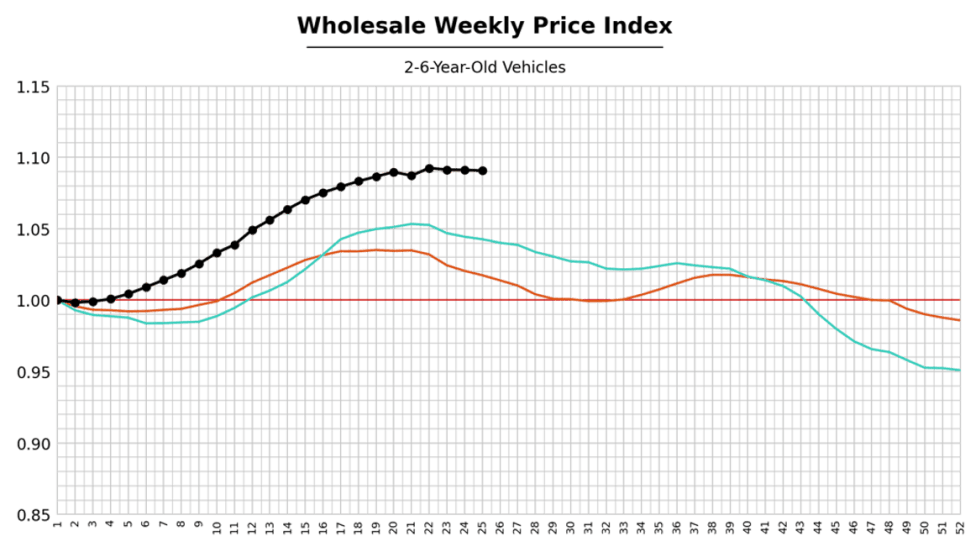

Black Book: Weekly Market Update

Wholesale automotive auction activity slowed noticeably last week, though business still remained healthy, analysts reported.

Read More →

Texas vs. California

The state known for its pickups penchant threatens to overtake the traditional center of U.S. car culture as it grows sales of new vehicles and pays more for them.

Read More →

Hybrids Record Highest Annual Mileage

A new study shows that conventional hybrids are the most heavily driven vehicles on the road, while plug-in hybrids are the least-driven power train.

Read More →

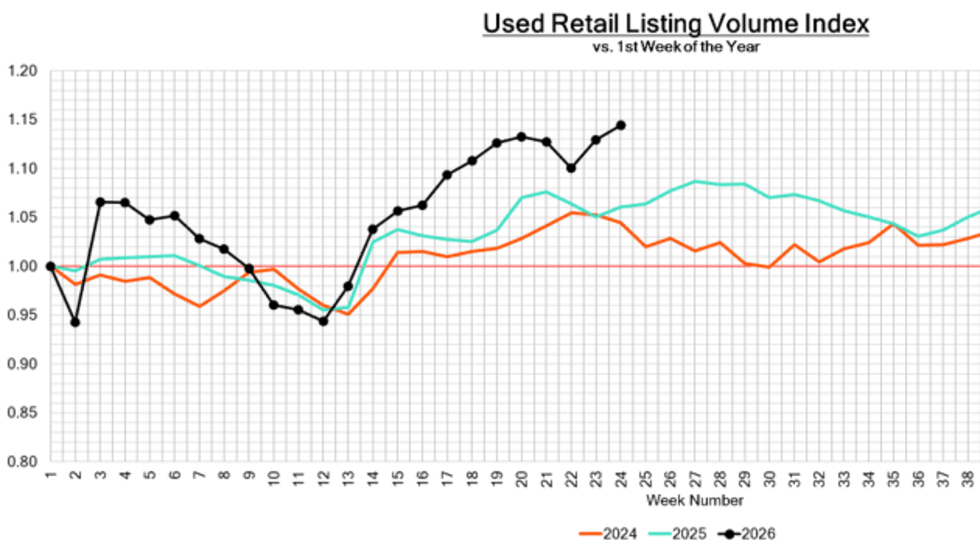

Black Book: Weekly Market Update

Last week's wholesale vehicle auction activity reflected seasonal patterns as buyers stayed choosy about selections, analysts reported.

Read More →

Auto Prices Ride May Moderation

Flat ATPs and asking prices clocked in below long-term averages for the month, though some segments saw significant price gains, reported Cox Automotive.

Read More →

Auto Retail Families Get Out While the Getting’s Good

Kerrigan Advisors’ first-quarter Blue Sky Report shows a sharp uptick in buy-sell deals as more retailers take advantage of handsome values while seeking to escape market risk.

Read More →

Holman Opens New Lexus Dealership

Located in the heart of Clark County, Lexus of Vancouver features a multi-level showroom, more than 30 service bays, an indoor drive for drop-off and pick-up and a fleet of courtesy vehicles.

Read More →

Ownership Priorities are Shifting

A new survey shows that in the U.S. vehicle quality for generation Z is largely defined by advanced safety features, intuitive technology and premium sound systems.

Read More →