Compliance

California’s New Enforcement Playbook for VSC Providers

Recent state insurance department regulator actions signal that it’s expanding regulatory risk for the VSC industry, whose players should prepare themselves for compliance.

Understanding the risks and benefits of retail accounting and Super CFCs can help you better present options to your dealer partners.

Not all retail accounting programs are structured in the same manner, and it's critical to understand how providers are managing programs’ costs and regulatory insurance compliance.

Pixabay/AymaneJed

Retail accounting is not a new concept. In fact, many providers and dealers have successfully used retail accounting for many years, most commonly in the form of third-party obligors and dealer owned warranty companies that offer vehicle service contracts.

This method of accounting is typically used by insurance companies, or entities treated as insurance companies for U.S. federal income tax purposes, to record gross written premium at retail cost, i.e., the customer purchase price. Retail accounting methodologies, in conjunction with statutory accounting principles, create the ability to potentially defer federal income taxes.

Let’s look at an example of how retail accounting can be used to defer federal income tax:

Obligor A sells 15,000 VSCs a year with an average term of 60 months. Each contract typically sells for $3,000, including $2,000 of commission retained by the dealership. For simplicity, we will assume no losses or other expenses. Using the retail accounting method at the end of year one, obligor A’s statutory income statement would look at follows:

Gross Written Premium: $45,000,000

Change in Unearned Premium: $(36,000,000)

Earned Premium: $9,000,000

Commission Expense: $(30,000,000)

Statutory Net Loss: $(21,000,000)

This fact pattern would result in a net operating loss for U.S. federal tax purposes of $13.8 million, inclusive of the necessary tax adjustments.

Ideally, obligor A would use the cash savings from deferring current federal income taxes, along with access to cash held to secure future claims and invest those monies at a rate higher than obligor A’s marginal tax rate. In other words, obligor A would use what is essentially an interest free loan from the U.S. government to invest in higher-yielding assets.

DOWCs that utilize the cash savings to fund acquisitions of additional producing dealerships could potentially maximize their returns twofold: first, by providing dealership principals with a source of capital with terms more favorable than traditional capital sources, and second, increasing production volume that typically extends the deferral period.

In its simplest form, a Super CFC is a licensed reinsurance company that utilizes retail accounting to defer U.S. federal income tax. A Super CFC will be too large to make a section 831(b) election and so shareholders are not concerned with keeping the annual written premium below the statutory cap.

A Super CFC offers some advantages over traditional obligors or DOWCs:

While a Super CFC offers tangible benefits over a DOWC, there are potential downsides. Due to the reinsurance nature of a Super CFC, the entire program should be reinsured through a licensed insurance carrier that has issued a first-dollar contractual liability insurance policy, or FD CLIP,” to an obligor.

As with any FD CLIP program, the premiums – customer cost in this case – are subject to premium tax. One could imagine the economic strain of subjecting the full retail cost to an average premium tax rate of 2%. Many providers have found economically viable ways to reinsure the premium with an FD CLIP, but it is important to understand how premium is reinsured to a Super CFC to avoid unnecessary tax and compliance risk.

Not all retail accounting programs are structured in the same manner, and it is critical to understand how providers are managing programs’ costs and regulatory insurance compliance. Additionally, as with any reinsurance arrangement, a collateral trust is typically involved, which can limit the investment options that could make it harder to achieve investment returns in excess of the marginal tax rate. Partnering with a CLIP provider that can offer solutions to these complex compliance issues is key to offering a successful Super CFC program.

Specifically, proper structuring should consider any exposure to issues associated with engaging in unauthorized insurance and additional taxes and fees for participating dealers.

Unauthorized insurance is any insurance provided by an entity that is not admitted or licensed in the state where the insured is located, which falls within each state's regulatory authority under the McCarran-Ferguson Act's delegation of insurance regulation to the states.

If an obligor procures coverage directly from a nonadmitted insurer, like a Super CFC, without using a surplus lines broker, most states impose a self-procurement, or independently procured, tax on the premium—in this case, the full customer cost.

Importantly, a risk-transfer agreement, particularly one structured to shift economic risk to an unlicensed offshore or affiliated carrier, could expose the parties to unauthorized insurance exposure if regulators recharacterize the arrangement as insurance being transacted in-state, triggering unpaid self-procurement taxes, penalties and potential enforcement action for unlicensed activity.

As the industry continues to see an increase in the adoption of Super CFC programs, providers and administrators should be aware of the complex issues that can arise as they work with CLIP providers, dealers, and trust and investment managers to bring new and innovative products to the market.

If you're currently evaluating whether a Super CFC structure makes sense for your dealer partners, or if you're already operating one and want to pressure-test its compliance posture —it is certainly a worthwhile endeavor to take a close look at the tax, licensing, and premium reinsurance mechanics underpinning the program. The margin for error on issues like premium tax treatment, collateral trust structuring, and FD CLIP design is narrow, and the regulatory landscape continues to evolve.

Ian Osler / Eli Colmenero

Morgan Miller Photography

ABOUT THE AUTHORS: Ian Osler is an insurance tax partner, and Eli Colmenero is an insurance tax manager, at MarksNelson Advisory, LLC – a Springline company.

EDITOR’S NOTE: This article was authored and edited according to Providers & Administrators’ editorial standards and style. Opinions expressed may not reflect that of the publication.

Loading data...

Compliance

Recent state insurance department regulator actions signal that it’s expanding regulatory risk for the VSC industry, whose players should prepare themselves for compliance.

Product & Technology

Data, video and artificial intelligence are driving service performance today, when inspection performance is closely tied to key business outcomes.

Awards

Buffeted by trial after trial as a young man, David Wright knew he’d found his life path when he stumbled into auto retail after all other doors slammed shut. The 2026 Time Dealer of the Year shares the lessons he learned along the way.

Industry

Understanding the risks and benefits of retail accounting and Super CFCs can help you better present options to your dealer partners.

Actuary

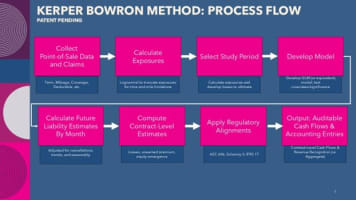

The Kerper Bowron Method is a patent-pending approach that builds on established actuarial principles but applies them at the individual contract level.

Industry

Providers and administrators should clearly and credibly communicate their experiences since their numbers will draw more scrutiny this year.

Compliance

In Trump’s first year, just 60,917 pages were printed in the Federal Register, the official journal of the federal government, down 42%.

Industry

As America turns 250, explore how the automotive industry shaped jobs, culture, innovation, and mobility from Detroit assembly lines to today’s EV era.