Black Book recently published an update to their weekly COVID-19 Market Insights report.

Here is a quick recap of industry related headlines over the last week:

Wholesale prices continued their decline last week at the seasonally normal rate, for the sixteenth week in a row.

Average retail listing prices of available inventory have been essentially flat over the last two months, but overall pricing began to show signs of softening over the last month, with larger declines occurring over the last three weeks.

Used retail listing volume continued to increase last week, but remains at levels lower than last year – about 3.9% below prior year, and 7.6% below where the industry began 2020.

“Nowcast” for annualized GDP growth rate in the fourth quarter is 10.4%, according to GDP Now’s forecast from the Atlanta Federal Reserve.

Weekly initial unemployment claims decreased, but stayed above eight hundred thousand, as noted in last week’s DOL report.

With the election behind, consumer sentiment increased in December “due to a large and rapid partisan shift, with Democrats becoming much more positive and Republicans much more negative”

CarMax, the largest used-car retailer, reported their results for the latest quarter ending on November 30th. Here are the highlights:

Total used units sold increased 1.0%, totaling 194,576 units sold, while used unit sales in comparable stores were down 0.8%

Gross profit per used unit of $2,151 was similar to the prior year quarter

Total wholesale units increased 10.8% – 126,317 units sold

Wholesale gross profit per unit decreased to $906 from $937 versus the prior year quarter

TransUnion’s November monthly industry report showed an overall improvement in the number of accounts in hardship, although sub-prime accounts are still slow to recover.

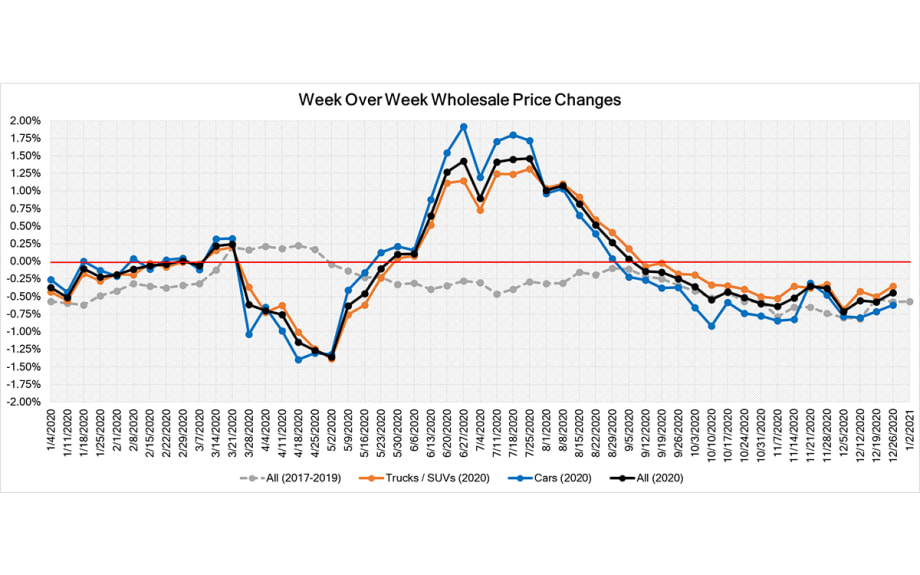

Last Week’s Highlights from the Wholesale Market

Volume-weighted, overall Car and Truck segments both experienced continued softening in values last week, but the rate of decline decreased compared to the prior week. The overall market decreased by –0.45% this past week (compared to –0.58% the prior week). As for specifics, the overall Car segments decreased –0.62% (compared to –0.72% the prior week), and the overall Truck and SUV segments decreased this past week at a rate of –0.35% (compared to a decrease of –0.50% the prior week).

The graph below shows week-over-week depreciation rates for the entire market, including Cars and Trucks/SUVs/Vans for the last several months. We also show an average weekly change versus several previous years (grey line).

News from the Retail World (Used and New)

New car demand has been fueled by heavy incentives as dealerships and OEMs push to finish out the year strong. Full-Size Trucks and SUVs continue to have strong demand, but large incentives are putting pressure on used values.

Used retail prices continue to soften as demand remains down to finish the year and used inventory levels grow.

There could be a new automaker in the mix by 2024. Apple announced they are reviving their plans to enter the auto market with a battery-powered vehicle.

As Britain faces a new strain of COVID-19 and borders close, the impacts are starting to hit the automotive industry. Toyota was forced to halt production in the UK and France. However, the good news is that it is only a small extension from the already planned holiday closures.

What Comes Next?

We are starting to see an incremental influx of used inventory coming to the marketplace, but with weakening demand, we saw a decrease of about 15% in the auction sales rate, compared to the Summer months.

It also appears that most of the lease returns and trade-in vehicles never make it to auctions, as grounding dealers are keeping the inventory for retail sales.

Most lenders have re-started the process of repossessions, at least on paper, as the economy continues to feel the effects of high unemployment, but the process is slow and the number of vehicles hitting the auction lanes is still insignificant.

All these factors contributed to the overall reduction (compared to the third quarter) in the number of vehicles sold on the wholesale market.

With COVID-19 cases and deaths increasing substantially across the country, we expect this weakness in demand and overall cautiousness by dealers to last well into 2021.

With much weaker retail demand and a projected increase of used inventory, we forecast a higher than seasonal drop in wholesale prices this winter. It is worth noting that after record breaking increases in wholesale prices over the summer, we are still well above pre-COVID-19 prices, so the projected drop over the winter months will simply get us back to the baseline.

Longer Term View

Although used vehicle supply will decline significantly due to cuts in lease and fleet (both rental and commercial) sales throughout 2020 and into 2021, the economic effects of the pandemic will continue to be felt as far out as three years from now (for example, the most recent quarterly Federal Reserve projections from September show unemployment above 4% for the foreseeable future), Black Book projects that wholesale vehicle values will decline to the pre-COVID-19 baseline in 2021 (from record highs during the summer of 2020) and will stay at these levels until at least 2023.

Economic Conditions

Job Market

The graph above compares weekly initial unemployment claims from the current recession against the Great Recession of 2007 – 2009. The severity and speed of job losses during this crisis is unprecedented. The horizontal (x) axis is an offset (in months) from the beginning of the recession, with week 0 being the week of March 21st.

Last week, the Labor Department reported that the US added 803,000 new jobless claims – an decrease of 89,000 from the revised prior week’s numbers.

Since the start of the pandemic in March, we have seen 40 consecutive weeks of record layoffs and furloughs, indicating that businesses are still struggling to start a full recovery.

In the early stages of the crisis, the US unemployment rate in April skyrocketed to 14.7%, the highest monthly rate since the Great Depression.

The May unemployment level decreased to 13.3% due to the success of the Federal Paycheck Protection Program (PPP) and other stimulus measures enacted in part by the Federal Reserve and Government.

As the country and economy continued to reopen during the early part of June, the monthly unemployment numbers eased further to 11.1% and dropped to 10.2% in July.

In August, we saw further improvement in the labor market as the unemployment rate fell to 8.4%.

The September unemployment number dropped to 7.9% mostly due to the exit of many workers from the employment pool. Additionally, job gains slowed down significantly.

In October and November, the economy continued to slowly recover, and unemployment rate dropped to 6.7% in November while job gains slowed down even further.

The Labor Bureau also noted in its reports that there was a classification error in its surveys, and the real unemployment numbers were higher for each month since March, as illustrated above.

This recession is very different and unprecedented in the labor market – reflecting an almost instantaneous jump in unemployment with projected fast growth and recovery within several years. The graph above compares unemployment rates for the last several major recessions. The horizontal (x) axis is an offset (in months) from the beginning of the recession.

Although we have seen a reduction in unemployment claims, the initial economic shock and job losses have created a deep hole for us to dig ourselves out of. Between February and the end of November, the nation lost close to 9.8 million jobs.

Consumer Confidence

Not surprisingly, consumer confidence has been on a rollercoaster over the last six months.

At the beginning of the year, sentiment was strong – the University of Michigan’s Monthly Consumer Sentiment Index in February was at 101 points.

As the COVID-19 pandemic spread across the US, the Index dropped to 71.8 points in April and increased slightly to 72.3 points in May.

During testimony by Federal Reserve Chair Jerome Powell, he noted that during the months of April and May, “stimulus checks and unemployment benefits are supporting household incomes and spending.”

With these one-time stimulus payments and extended unemployment benefits helping the economy, the Index for June increased further to 78.1. The gains, however, were not uniform across the country. With a significant reduction in the number of COVID-19 cases, the Northeast region led the way with a record 19.1 points month-over-month jump, while the Southern region rose just 0.5 points due to the dangerous increase in numbers of new infections and fear of further shutdowns.

With the weakening of the economy, and the increase in new COVID-19 cases across the South, consumer confidence retracted to the lows of April in July. The University of Michigan’s Monthly Consumer Sentiment Index for July decreased to 72.5 points and increased slightly in August to 74.1.

The September Index increased further to 80.4, but still remains heavily depressed compared to pre-COVID and last September’s numbers.

Final numbers for October stood at 81.8 – a slight improvement since September and the highest point since April’s drop.

As number of cases and deaths surged across the country, consumer confidence slid to 76.9 in November.

With the election behind, consumer sentiment increased to 80.7 points in December “due to a partisan shift in economic prospects. Following Biden’s election, Democrats became much more optimistic, and Republicans much more pessimistic, the opposite of the partisan shift that occurred when Trump was elected”.

Gross Domestic Product (GDP)

The Bureau of Economic Analysis (BEA) published the third estimate of GDP in the second quarter (as of September 30th) – real GDP decreased at an annual rate of 31.4%. This was the highest drop in GDP ever recorded.

BEA’s advanced estimate for third quarter showed an increase in real GDP at an annual rate of 33.1%.

The current “nowcast” from the GDP Now model [from the Federal Reserve] estimate for real GDP growth (seasonally adjusted annual rate) in the fourth quarter of 2020 was 10.4% on December 23rd.

Delinquencies in Automotive Lending

The number of accounts in ‘hardship’ jumped substantially in April, and kept increasing through June across all risk groups, according to the Monthly Industry Snapshot by TransUnion. The numbers stabilized in July and improved in August through November. In November, about 3.2% of all accounts were in hardship – this was roughly a 520% increase over last year. The increases were across all risk tiers. As deferrals expire in the upcoming months, coupled with a high unemployment rate, lenders expect a large portion of these ‘hardships’ to become delinquencies.

The numbers are substantially higher for subprime tiers – as of November, about 10.4% of all subprime automotive accounts were in hardship – a relative stability since August.

According to the “Senior Loan Officer Opinion Survey on Bank Lending Practices” from the Federal Reserve, lenders tightened standards on auto loans during first three quarters of 2020.

The Board of Governors of the Federal Reserve System released results from the fourth quarter that showed even more tightening of their standards for auto loans.

Fuel Prices

Since their lowest point at the end of April, gasoline prices are up $0.45, to $2.24 per gallon last week, a seven cent increase from the prior week, according to the U.S. Energy Information Administration.

After dropping by $0.70 in the Spring, diesel prices remained relatively flat through the Summer and Fall months, below $2.50 per gallon. We started to see the increase in December. Last week prices went up by six cents to $2.62 per gallon.

Current Wholesale Market Overview

Auction Insights

Last week was a quiet week for many auctions as dealers weren’t in need of much inventory due to the recent weak retail demand. Sellers were also holding firm to floors in hopes that the new year will bring stronger demand. Due to the slow demand and sellers’ firmness on floors the sales rates declined leading up to the holidays.

For many remarketers we’ve talked to it is their sentiment that inventory’s are low so they are willing to wait to see if January will bring back the demand that was experienced over the summer. However, they do have mixed feelings on expectations of a traditional tax/spring season market bump.

Auction Volume

Over the last several weeks we have seen wholesale sold volume decrease as dealers started to pull back on purchasing.

The drops in volume were not uniform across all auctions and platforms.

We saw a significant drop in sold volume (both month-over month, and year-over-year) in wholesale channels from September to November. There are several factors that contributed to this drop:

The no-sale rate increased substantially during the Fall (by about 15%), as many remarketers were not willing to adjust price floors.

We also saw a decrease (YOY) in available units:

Rental companies held back some units to cover Hurricane related rentals in September and October.

They sold lower volume in November as purchases of new models are being pushed into 2021.

Repossessions are slow to hit the market, as the process has slowed down significantly compared to pre-COVID days.

Dealers are holding on to more trade-ins and lease returns compared to previous years.

The graph below illustrates the estimated year-over-year change in the monthly sold volume within the wholesale market. The summary includes all major wholesale channels, including open auctions (digital and physical), dealer-to dealer platforms, direct to dealer sales, etc.

Sales Rate

At the onset of the pandemic, shelter-in-place orders took effect and sales rates quickly tumbled into the teens.

Subsequently, rates began climbing each week before finally stabilizing in June and July.

After months of consistently strong sales, much of these seller’s best inventory was sold, and retail demand began to soften in certain segments. As a result, sales rates started to decline in August leading up to Labor Day.

Sales rates stabilized in September and October as sellers adjusted floors to reflect the weakening wholesale values.

Heading into the Thanksgiving holiday, with COVID-19 cases sending many areas around the country back into lockdown, we saw the weaker retail demand leading to lower demand on the lanes and increases in no-sales. Post-Thanksgiving, the sales rates increased as buyers still need inventory after the successful summer months and sellers were more willing to negotiate.

Similar to the trend seen around Thanksgiving, leading up to the end of the year and the holidays, with dealer inventory growing as retail demand started to decay, auctions have begun to see lower sales rates.

Black Book’s estimate of the overall Weekly Average Sales rate is presented below.

Current Wholesale Price Trends

Current Market Level View

Volume-weighted, overall Car segment values decreased -0.62% over the last week, a decrease from the depreciation of –0.72% experienced the week prior.

Compact Cars continue to be on a downward slide. This now marks eighteen straight weeks of declines for an average of –0.92% per week.

Sporty Cars and Luxury Cars also had large declines this past week, both exceeding –0.70%.

The surprise throughout the pandemic has been the stability of the Premium Sporty Car segment, which continued to have relatively low depreciation this past week at only –0.17%.

When volume-weighting is applied, the overall Truck segment (including pickups, SUVs, and vans) values declined -0.35% last week, a decrease in depreciation compared to the previous week’s change of –0.50%.

Minivans have consistently been leading the declines each week and this past week was no different. This marks the sixteenth week of declines for an average depreciation of –0.72% per week.

With heavy incentives on Full-Size Trucks, the values have been experiencing consistent weekly depreciation. This past week the segment declined –0.40%, compared to –0.38% the week prior.

Black Book’s Seasonally Adjusted Retention Index

The graph above compares Black Book’s Seasonally Adjusted Retention Index for 2019 and 2020 calendar years. The Black Book Used Vehicle Retention Index is calculated using Black Book’s published Wholesale Average value on two- to six-year-old used vehicles, as a percent of original typically equipped MSRP. It is weighted based on registration volume and adjusted for seasonality, vehicle age, mileage, and condition. The Index offers an accurate, representative, and unbiased view of the strength of used vehicle market values. It measures an ‘apples-to-apples’ year-over-year retention comparison.

2020 started slightly below 2019 levels, but the market showed early strength in February and March.

As the US economy shut down due to the COVID-19 pandemic, we measured the highest single month drop in April of 6.9 points since launching the Index.

As we entered July, wholesale prices continued the rebound that began during the second half of May and continued through the month of June, with June’s Retention Index climbing back to pre-COVID-19 levels with a record jump of 9.1 points.

Black Book’s July Index value jumped above 2019 to 126.0 points as wholesale prices continued their climb.

August Retention Index jumped further to 129.0 points – the highest retention level ever recorded since the inception of the Index in 2005.

Our September index came at 130.8, a – 1.4% increase from August and 12.8% higher than in 2019. Market strength was driven mostly by the Full-Size Pickup segment.

The October market Index was again helped by the strength of the Full-Size Pickup segment – Index dropped slightly (0.7%) from September to 129.9.

In November prices depreciated at a slower than seasonal rate which led to a small increase in the Index by 0.7 points to 130.6.

Our “nowcast” for December shows an essentially flat Index at 129.9 points.

During the last recession (2007-2009), the Index declined by about 15 points in a span of 12 months before a recovery started. We project that the Index will decline over the next five months after experiencing the summer’s strength. The graph below shows the historical trends in the Black Book Retention Index that covers the last 15 years, including the Great Recession.

Used Wholesale Price Projections

Wholesale Price Impact Under the Most-Likely Economic Scenario

2020 In Review

The wholesale market started the year strong from January through March, as prices increased during the first quarter.

Wholesale prices dropped significantly in April, as uncertainty over COVID-19’s impact and response dampened vehicle demand. This resulted in an overall wholesale price decline of 5.9%.

We saw a substantial improvement in prices during the last two weeks of May as many states re-opened their economies, and the monthly decrease was limited to only -1.5%.

During the summer months, demand in the automotive market was fueled by federal government stimulus and delayed tax season. Additionally, used and new inventory shortages drove wholesale prices up.

In June, wholesale prices continued to increase, and the overall market appreciated by 5.7%. As a comparison, last year’s prices declined by 0.9% over the same period.

Wholesale prices increased by a record 7.0% in July.

Wholesale prices continued their ascent in August and increased by an additional 2.7%.

Prices started to decline during the first week of September and declined by 1.0% by the end of the month. Performance varied by segment with the strength coming from Full-Size Pickups (which increased by 1.2%).

In October, we saw overall seasonal price declines of 2.7%, on par with previous years. It is worth noting that without the strength of the Full-Size Pickup segment, the average price decline would be steeper.

Overall depreciation in November slowed down a little to 2.1% due to continued strength in the Full-Size Pickup segment.

Short-Term Outlook

The graph above shows a market level weighted average projected (dashed lines) and historical (solid line) wholesale values for all 2017 model year models.

We project a continuous drop in wholesale prices through the winter, as the US economy suffers through the effects of COVID-19, and due to an increasing used supply. Prices will start to go back to “normal” seasonality in the second half of 2021 as the economy becomes stronger and supply shrinks.

We also anticipate that older (>6-year-old), cheaper vehicles in average condition will not decline as much due to increased demand for these units.

Long-Term Projections (36-Month Residual Values, Fall / Winter of 2023)

The economic effects of the pandemic will continue to be felt out to 36 months from now. We project values will return to the pre-COVID-19 baseline as used supply will decline due to cuts in retail and fleet sales throughout the remainder of 2020 and into 2021.

Used Retail Vertical

Used Retail Prices

With the proliferation of ‘no-haggle pricing’ for used-vehicle retailing, asking prices accurately measure trends in the retail space.

From the peak in early April, until the end of June, retail listing prices decreased by about 4%.

Starting in the second week of June, we saw an increase in used retail prices fueled by higher consumer demand due to stimulus payments, the federal Paycheck Protection Program (PPP), and limited used and new inventory.

By early August, used retail prices rebounded to above pre-COVID-19 levels.

We started to see some weakness and decline in retail prices in November.

We expect used retail prices to decline this winter as demand will continue to soften during a weak economy.

Used Retail Inventory

Many dealers continue to report a shortage of used inventory in the wholesale marketplace. As a result, from the peak in February, we have seen a decline in the number of used retail listings by between 20% and 25%. Current inventory level is about 7.6% below where we started the year and slowly growing.

The true shortage of vehicles is probably not as severe as this decline would lead you to believe, as many dealers sell some of their best inventory in the first several days before listing them online. Nevertheless, the shortage of used inventory helps keep retail prices elevated, even in the weak economic conditions.

The graph above shows the weekly average of the number of retail listings collected by Black Book, indexed to the first week of the year. We see a continuous decline in the numbers starting at the beginning of May as the economy started to open in the states outside of the Northeast.

The graph below shows year-over-year change in average monthly retail listings.

We started 2020 with active retail listings above previous year’s levels.

By July, the listing volume dropped to about 7% below 2019 numbers.

August saw another drop in listed inventory to about 9% below 2019.

In September, inventory listings continued to grow and were about 6% below 2019.

In October the number of listings continued to rebound and were about 1.8% lower compared to last year.

Currently, the week of Christmass holiday, inventory levels are about 3.9% lower, year-over-year.

Used Retail vs. Wholesale Prices Trends

Each week, members of the Black Book automotive analyst team, data science team and executive leadership team speak with no less than 30 dealers, along with buyer and seller representatives, wholesalers and others, who represent hundreds of franchise and independent dealers nationwide. These industry experts, along with experts we speak with from leading fleet management and rental car companies, auction leadership, and other industry experts, help to clarify and connect the dots between the wholesale and retail markets, adding to the insights that our data reveals.

Since the start of the pandemic, we have been observing different trends in both wholesale and retail prices (see graph below).

In April and May, wholesale prices declined at a higher rate compared to retail prices. As margins grew, dealers reported healthy profits on a per vehicle basis. Retail prices displayed stickiness on the way down.

Similarly, as wholesale prices came roaring back to pre-COVID-19 levels in July and August, retail prices were slow to recover, exhibiting the same stickiness on the way up.

As the wholesale market started to decline in September and October, we began to experience the early stages of our expectations that both wholesale and retail (outside of the Full-Size Pickup segment) prices will decline significantly over the remaining months of 2020.

The graph below captures this retail / wholesale dynamic since the start of the year. Prices are indexed to the first week of the year. The black line is Black Book’s Retention Index (not adjusted for seasonality). It is calculated using Black Book’s published Wholesale Average value on two- to six-year-old used vehicles, as a percent of original typically equipped MSRP. It is weighted based on registration volume and adjusted for vehicle age, mileage, and condition. The blue line is the retail index – the average listing price of available retail inventory adjusted for mileage.

New Vehicles Sales Outlook

We still anticipate a significant reduction in US new vehicle sales in 2020 (both retail and fleet sales) due to a continued reduction in consumer demand. This is the result of several ongoing factors, including less miles driven due to remote work and shelter-in-place initiatives, high unemployment, and an overall feeling of uncertainty by consumers.

Overall, new vehicle sales were down 17% during the first eleven months of the year compared to last year (with a 6% YOY increase in September and 1% increase in October mainly due to strong retail sales and 15% drop in November).

Our New Vehicle Sales Outlook was updated based on stronger than expected August through October sales numbers. Due to continuous production disruptions, and much weaker demand due to the economic slow-down, we project at most 18% drop (compared to pre-COVID-19 projections) in new sales in 2020 to at least 13.9mm units in our base economic scenario.

In the longer-term, we expect new sales volume to return to pre-COVID-19 levels within five years.

Used Vehicle Supply Projections

Black Book projects a modest increase in used vehicle supply in the wholesale marketplace in the first half of 2021 due to increased repossessions due to deteriorating economic conditions in addition to delayed repossessions during spring and summer months. This additional volume could exceed half a million additional units in 2021 (compare to a “normal” 2019).

The second half of the year will see normal overall level of used vehicle supply, although the mix of vehicles maybe different: lower number of newer used rental returns but elevated volume of older repossessed vehicles.

Repossessions

About 1.9 million vehicles were repossessed by lenders and sold (mostly) through wholesale channels in 2019. During the beginning of the pandemic, most states put a moratorium on auto repossessions and most lenders had deferral programs to help owners through the first several months of the recession. Most of the lenders have ended their deferral programs. Our survey of lenders and automotive recovery companies suggest that the volume of repossessed vehicles will at least double in the next six months. We expect that there will be substantial challenges at every step of the process as recovery, transportation, and disposal are not fully recovered.

Rental Unit Returns

Business and leisure travel collapsed at the end of March – air travel is still down by more than 60% according to the TSA. In addition, there is no expectation that travel will return to pre-COVID-19 levels over the next several years. According to the IATA (International Air Transport Association), air travel will not return to pre-COVID-19 levels until after 2024. This puts tremendous financial pressure on rental companies that rely on air travel to reduce both their current fleet and scrutinize future vehicle acquisitions.

At the end of May, Hertz filed for bankruptcy in North America as a result of the pandemic. Hertz was able to secure a deal with its lenders that allows a gradual reduction of fleet – over 182,000 units between June and December. In addition to Hertz, other rental companies reduced their fleet during the summer and fall months to match lower demand for rentals. This practice lead to over 250,000 additional rental units on the wholesale market in the second half of 2020.

In the longer term (later 2021 – 2023), the drop in rental return volume will benefit the price of newer used units, as supply will be limited.

Longer Term Used Returns Projections

With the reduction in retail and fleet sales over the next several years, we project a substantial decrease of available used inventory in the years to come. The graph below illustrates the numbers of returned vehicles up to 8-years-old. This lower level of used inventory will be beneficial to used car prices as supply will be limited, helping to bolster valuations.