Wholesale Prices, Week Ending August 13th

Black Book: Weekly Market Insights

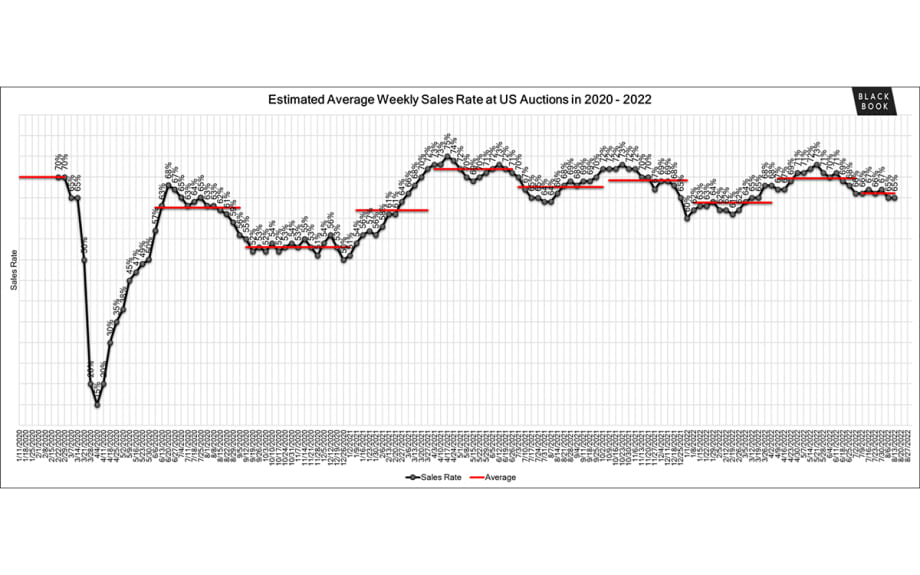

The Estimated Average Weekly Sales Rate remains at 65%.

August 17, 2022

The Estimated Average Weekly Sales Rate remains at 65%.

5 min to read

Large overall market declines continued last week, far exceeding the levels that are expected for this time of year. The luxury segments are leading the way, but other volume segments, such as Compact

This Week Last Week 2017-2019 Average (Same Week)

Car segments -0.90% -0.92% -0.15%

Truck & SUV segments -0.82% -0.88% -0.19%

Market -0.85% -0.89% -0.18%

Car Segments

On a volume-weighted basis, the overall Car segment decreased -0.90%. For reference, the previous week, cars decreased by -0.92%.

All nine Car segments decreased last week.

Luxury segments continued to experience large depreciation last week. The Prestige Luxury Car segment reported the largest decline at -2.00%, following the prior week’s already large decline of -1.34%.

The Compact Car segment continued the declines last week, but the rate of decline lessened to a decrease of -0.67%, compared with the prior week’s -1.06%.

Truck / SUV Segments

The volume-weighted, overall Truck segment decreased -0.82%, compared to the prior week’s decrease of -0.88%.

All thirteen truck segments reported decreases.

Full-Size Vans have been on a downward slide after over a year of increases, but the rate of declines leveled off last week, with the segment reporting a minimal decrease of -0.05%.

Sub-Compact (-1.63%) and Full-Size (-1.60%) Luxury Crossover/SUV segments experienced the largest Truck market declines last week. Both segments however, slowed the rate of depreciation compared to the prior week with declines of -1.90% and -1.71%, respectively.

Weekly Wholesale Index

Calendar year 2020 and 2021 ended with used wholesale prices at elevated levels. With economic patterns (including the automotive market) driven by the pandemic, normal seasonal patterns (e.g., 2019 calendar year) in the wholesale market were not observed for most of the last 2 years. We saw a similar picture in 2009, at the end of the Great Recession. Calendar year 2021 did not have typical seasonality patterns as the market had rapid increases in wholesale values for the majority of the year. The Wholesale Weekly Price Index reached the highest point of the year at the end of December 2021, reporting over 1.51 points. Throughout 2022, the Index has remained stable compared to the beginning of the year.

The graph below looks at trends in wholesale prices of 2-6-year-old vehicles, indexed to the first week of the year. The index is computed keeping the average age of the mix constant to identify market movements.

Retail (Used and New) Insights

Rivian is aiming to increase their output at their assembly plant in Illinois by adding a second shift. The plant is capable of 150,000 unit per year, but the first half of 2022 yielded less than 7,000 units.

Toyota was forced to shut down their Tsutsumi plant for two days last week, due to the spread of COVID. Despite numerous closures in 2022, the automaker is confident in their ability to hit their production goals for the year.

Acura began teasing their all-electric concept vehicle that is set to be debuted in Monterey on August 18th. The Precision EV Concept vehicle is not expected to be available until 2024.

Polestar is preparing for their first crossover to be launched next year. The mid-size crossover will be the brands second volume model and will be named Polestar 3.

Used Retail Prices

Used Retail Prices are more accessible than in years past, due to the proliferation of ‘no-haggle pricing’ for used-vehicle retailing. Transparent pricing upfront makes the car buying process more enjoyable for customers and allows Black Book to accurately measure retail market trends.At the on-set of the pandemic, in CY2020, used retail prices increased slightly, following typical seasonal patterns, and then began dropping in April, finally hitting a low point in the late spring months. By late summer of CY2020, Used Retail Prices increased as supply of new vehicle inventory started to become scarce, but retail demand slowed down at the end of CY2020, resulting in declining retail asking prices for the last several weeks of the year. When CY2021 kicked off, demand rebounded while retail prices lagged slightly behind wholesale prices; March of 2021 started the dramatic increases in Used Retail Prices, fueled by stimulus payments, tax season, and shortages of new inventory. During the third quarter, retail prices continued to rise at a slower rate but soon picked up the pace once again to start the fourth quarter. In Q4, prices on retail listings steadily increased week after week. As CY2021 came to an end, the retail listing price index closed 36% above where the year began.

So far in 2022, the Retail Listings Price Index has remained relatively unchanged. The Index sits around 0.99, indicating a very slight decrease in retail pricing compared to the start of the year. Typically, there is a lag between changes in wholesale prices and retail prices.

This analysis is based on approximately two million vehicles listed for sale on U.S. dealer lots. The graph below looks at 2-6-year-old vehicles. The Index is computed keeping the average age of the mix constant to identify market movements.

Inventory

Used Retail

Used Retail Listing Volume has increased slightly as demand for used vehicles weakened.

The Used Retail Days-to-Turn Estimate has increased over the last month and now sits at 42 days.

Wholesale

The wholesale channels have remained consistent the past two weeks, with more model year 2022 vehicles available throughout the lanes, as well as newer used vehicles (model year 2019 to model year 2021). The condition of these vehicles has been average but with higher mileage. Smaller franchise dealers took advantage of the absence of the larger independent dealers and were very active in the lanes last week. Sales rates were stable, but inventory is still on the lower side as sellers’ floors are continuing to soften. Fuel prices are still decreasing, but that does not seem to help with the demand, as the market is still on a downward trend, showing signs of weakness. In the Car Segments, Prestige Luxury took the biggest hit, followed by Near Luxury, Luxury, and Sporty Cars. In the Truck Segments, Sub-Compact Luxury fell the hardest, followed by Full-Size Luxury, Compact Crossover, and Mid-Size Crossovers.

The Estimated Average Weekly Sales Rate remains at 65%.

Originally posted on Auto Dealer Today

More Dealer Ops

Franchises, Throughput Down in First Half

A handful of states see franchise growth through June, while EV sales per store boost overall business in U.S.

Read More →

Buy-Sells Up in Q2

Kerrigan metrics show there’s plenty of demand, though many sellers are waiting to pull the trigger.

Read More →

DOWC Powers the Future of F&I for NESNA

Company is providing a fully integrated F&I administration model to Nissan Extended Services North America’s dealer network.

Read More →

March New-Vehicle Sales Healthy

Despite incentive spending not keeping pace with deliveries volume, consumers make their purchases ahead of tariffs impact.

Read More →

New DOWC Program Debuts

Hybrid solution combines benefits of reinsurance and dealer-owned warranty companies.

Read More →

Dealer Survey Finds Anxieties

Kerrigan Advisors poll shows percentage of retailers expecting lower profits, valuations is on the rise.

Read More →

Calif. Dealer Group Challenges Scout Direct Sales

Says VW unit’s plans to sell directly to consumers violate state law.

Read More →

Six Powerful Questions

Take the time to answer these and lay the groundwork for a successful year-end.

Read More →

Autumn Analysis

Consider taking the change of the seasons as a cue to evaluate some key operational aspects of the dealership.

Read More →

Maximizing Revenue Potential

The strategic imperative for auto dealers is to prioritize F&I product sales and wealth-building in challenging times.

Read More →