Wholesale Prices, Week Ending May 27

The market continued to decline last week, the truck segments reporting an acceleration in the rate of depreciation and the largest single week decline since late January. The full-size van segment reported the largest decline since 2019, but the values remain elevated, many still surpassing original MSRP.

This Week Last Week 2017-2019 Average (Same Week)

Car segments -0.11% -0.16% -0.33%

Truck & SUV segments -0.32% -0.12% -0.09%

Market -0.25% -0.13% -0.19%

Car Segments

On a volume-weighted basis, the overall car segment decreased 0.11%. For reference, the previous week, cars decreased by 0.15%.

Three of the nine car segments increased last week.

After 18 weeks of increases, for an average weekly gain of 0.58%, the sporty car segment declined 0.19% last week.

Prestige luxury car reported the largest decline for cars, down 0.33%, consistent with the previous three weeks, which have averaged a 0.33% decline each week.

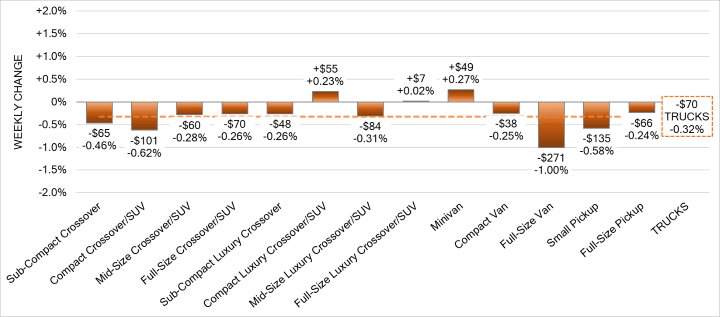

Truck / SUV Segments

The volume-weighted overall truck segment decreased 0.32%, compared with the prior week’s decrease of 0.16%.

Three of the 13 truck segments reported increases.

A popular summer travel segment, minivans (+0.27%) continued to report gains for the 15th consecutive week, with an average weekly increase of 0.60%.

Full-size van had the largest decline, 1.00%, its steepest drop since 2019.

Weekly Wholesale Index

The graphic below looks at trends in wholesale prices of 2- to 6-year-old vehicles, indexed to the first week of the year. The index is computed keeping the average age of the mix constant to identify market movements.

Calendar years 2020 and 2021 ended with used wholesale prices at elevated levels. With economic patterns driven by the pandemic, including the automotive market, normal seasonal patterns in the wholesale market, e.g., the 2019 calendar year, were not observed for most of the last three years. We saw a similar picture in 2009 at the end of the Great Recession. Calendar year 2021 did not have typical seasonality patterns, as the market had rapid increases in wholesale values for most of the year. The Wholesale Weekly Price Index reached the highest point of the year at the end of December 2021, reporting over 1.51 points. In 2022, the price index was on a mild rollercoaster until July, after which point, prices were on a continuous decline until the end of the year.

Used Retail Prices

Used retail prices are more accessible than in years past due to the proliferation of "no-haggle pricing" for used-vehicle retailing. Transparent pricing upfront makes the car-buying process more enjoyable for customers and allows Black Book to accurately measure retail market trends.

At the onset of the pandemic, in CY2020, used retail prices increased slightly, following typical seasonal patterns, and then began dropping in April, finally hitting a low point in the late spring months. By late summer of CY2020, used retail rrices increased as supply of new-vehicle inventory started to become scarce, but retail demand slowed at the end of CY2020, resulting in declining retail asking prices for the last several weeks of the year. When CY2021 kicked off, demand rebounded while retail prices lagged slightly behind wholesale prices; March 2021 started the dramatic increases in used retail prices, fueled by stimulus payments, tax season and shortages of new inventory. During the third quarter, retail prices continued to rise at a slower rate but soon picked up once again to start the fourth quarter, when prices on retail listings steadily increased week after week. As CY2021 came to an end, the retail listing price index closed 36% above where the year began. The index then remained relatively stagnant through most of CY2022. In the fourth quarter of 2022, the Retail Listings Price Index declines started but were not as steep as the wholesale price index.

This analysis is based on approximately two million vehicles listed for sale on U.S. dealer lots. The graphic below looks at 2- to 6-year-old vehicles. The index is computed keeping the average age of the mix constant to identify market movements.

Inventory

Used Retail

The Used Retail Active Listing Volume Index reverted back to one at the start of the year. Currently, the index sits at 0.99 points.

The Used Retail Days-to-Turn estimate is currently about 52.

Wholesale

For the second week in row, auction conversion rates were stable. With a holiday mixed in and Americans now starting their summer vacations, we saw little change in sales rates over the past weeks. 2500-3500 series truck prices continued to drop slightly more this week, while the 1500 series units saw relative stability. The car segments experienced downward movement but as much as the truck segments.As always, the Black Book team will continue to monitor and report on developing trends.

The Estimated Average Weekly Sales Rate remained at 48%.