Strong Consumer Credit Health Amid Economic Uncertainty

Despite challenges, TransUnion’s Credit Industry Insights Report shows consumer health and demand for new vehicles remains strong.

Despite challenges, TransUnion’s Credit Industry Insights Report shows consumer health and demand for new vehicles remains strong.

IMAGE: Getty Images

“It’s a puzzling time,” says Satyan Merchant, senior vice president and automotive business leader at TransUnion, as he leads a discussion on the latest auto loan trends from TransUnion’s Credit Industry Insights Report (CIIR).

Heightened demand and tightened inventory due to parts shortages and supply chain challenges has driven vehicle prices sky high. J.D. Power and LMC Automotive predict the average new-vehicle transaction price will hit a record $44,832 in May, an increase of $6,577, or about 16%, compared to May 2021.

Recently, inflation reached 8.3% and J.D. Power and LMC Automotive expect the average auto-loan interest rate to hit 4.92% in May, up 62 basis points or 0.62 percentage points versus 2021.

The CIIR Auto Loan Summary finds origination volumes in the fourth quarter of 2021 dropped to 6.5 million — a decrease of 3% over the same period in 2020. As a result, available vehicles fly off the lots even as vehicle affordability decreases.

“All this creates anomalies on the automotive finance side,” Merchant says. “There are so few vehicles available that originations are slowing. But credit is still available. This is not like 2009, when lending institutions pulled back because they were in trouble. Banks are not in crisis. They simply have no vehicles to lend against.”

Loan Payments and Terms Increase

The CIIR report finds average new auto loan amounts hit $28,415, a year-over-year increase of 15.2%. This change has pushed the average monthly payment of vehicle purchases (for both new and used vehicles) to $556, an increase of approximately $100 during a four-year period.

“Supply shortages have driven up vehicle prices and the shutdown of international factories will lead to a growing lack of inventory throughout the rest of the year,” Merchant says. “On top of increasing vehicle prices, rising inflation will also impact consumer purchasing power. We expect some lenders to offer lengthened loan terms to offset affordability challenges.”

Currently, the average term for an auto loan is 70 months. “That has remained steady for about five years,” he says.

However, TransUnion data shows the prevalence of longer terms is increasing. Eighty-four-month terms comprised 18% of new vehicle loans in the fourth quarter of 2021, compared to 16% the same quarter of 2020 and 13% in 2019. Used vehicle term lengths also increased. The average term is now 67 months versus 65 months a year ago.

“As interest rates go up, it’s going to put even more pressure on extended terms, just to keep monthly payments manageable,” he says. “It also will be interesting to see the terms lenders put on electric vehicles. EVs are far simpler vehicles from a mechanical point of view. If batteries can last 10 to 15 years, will terms go longer for EVs?”

Delinquencies Under Pre-Pandemic Levels

Despite inflationary pressures, personal loan delinquencies remain below pre-pandemic levels, adds Merchant. Consumers, he says, emerged from the pandemic with lower liquidity levels, giving them extra cash to put toward debt.

“Yes, we are in an inflationary environment. Yes, things are more expensive, autos included. However, consumers remain able to pay their debts,” Merchant says. “That’s why we see fairly steady delinquency rates in the auto sector and other lending lines.”

However, the serious delinquency rate (60_DPD) at the borrower level ticked up in the first quarter of 2022, increasing from 2.68% to 3.25% year over year. The report attributes the change to a growing share of balances held by below prime consumers.

“The subprime consumer is coming back,” Merchant says. “In 2020, they were really hurting. Many people weren't allowed to work during the pandemic. Now subprime consumers are showing some strength in vehicle sales and vehicle financing.”

Merchant attributes the slight uptick in delinquency to lower originations.

“Subprime borrowers are not showing any sort of spike in cumulative delinquency as compared to previous years,” he says. “Loan performance on the auto side has been unaffected. This means nothing out of the ordinary is happening.”

Balances Up

As delinquency rates remain well below pre-pandemic levels, total balances hit a new high of $178 billion in the first quarter of 2022 and grew 23.8% year over year, the fastest rate of growth since the second quarter of 2016.

“The growth was driven by a 12.2% year-over-year increase to the average balance per customer, which reached $9,896 in Q1 2022,” he says. “The number of consumers carrying a balance also grew for the third consecutive quarter to 20.4 million, just below the peak of 20.9 million consumers in the first quarter of 2020.”

Inflationary pressures will drive continued growth across all risk tiers as consumers seek credit to finance specific purchases or consolidate debt, but rising interest rates and economic uncertainties could dampen this growth, adds Merchant.

“Lenders will continue to monitor performance of subprime and near-prime consumers across their portfolios for signs of deterioration as they continue to lend in this segment,” he says.

New Product Strategies

Lenders must develop a product strategy as they face off against a challenging loan origination environment during a period of high demand, according to Merchant.

“Lenders must examine how they underwrite consumers and make the most informed decision possible on every application,” he says, “because cars are scarce. They don’t want to make the wrong decision on a loan.”

He also notes inclusion and efforts to close the equity gap will require a change.

“Lenders need to consider how they create and provide access to all communities and all types of people,” he says.

The shift will require lenders to focus on alternative data sets when making lending decisions.

“Many of these individuals don't have a mortgage, so lenders must base lending decisions on other criteria. Do they pay for their utilities on time? Do they pay their rents on time? Do they pay for a health club membership every month?” he asks. “TransUnion is working on improving access to alternative datasets so that lenders can make more informed decisions and provide safe access to credit to a wider population.”

Merchant adds more lending steps also must become available online. TransUnion surveys show consumers want to do more of the process online.

“They want to understand their monthly payment and work out their loan terms online. They want to walk into a dealership to pick up their vehicle or have the dealership deliver it,” he says.

Auto refinance also provides an opportunity right now. As gas prices rise, consumers at higher rates may want to refinance at a lower rate so save some money, he notes.

Risks Moving Forward

Everything looks great, but it’s not all coming up roses. Inflation and economic uncertainty will drive risk into a healthy credit market, Merchant stresses.

“It will be important for lenders to monitor signals across the consumer’s wallet and the overall consumer picture,” he says. “They need to know how consumers manage their credit obligations across the board.”

But for now, things still look good, even as the Federal Reserve raises interest rates. Employment holds strong and consumers have healthy finances, he concludes.

Ronnie Wednt is an editor for F&I and Showroom.

More Industry

Ownership Priorities are Shifting

A new survey shows that in the U.S. vehicle quality for generation Z is largely defined by advanced safety features, intuitive technology and premium sound systems.

Read More →

Pump Price Jump Calculated

ISeeCars.com examined fuel costs for different power trains, finding which ones have experienced the biggest hits since the war in Iran commenced.

Read More →

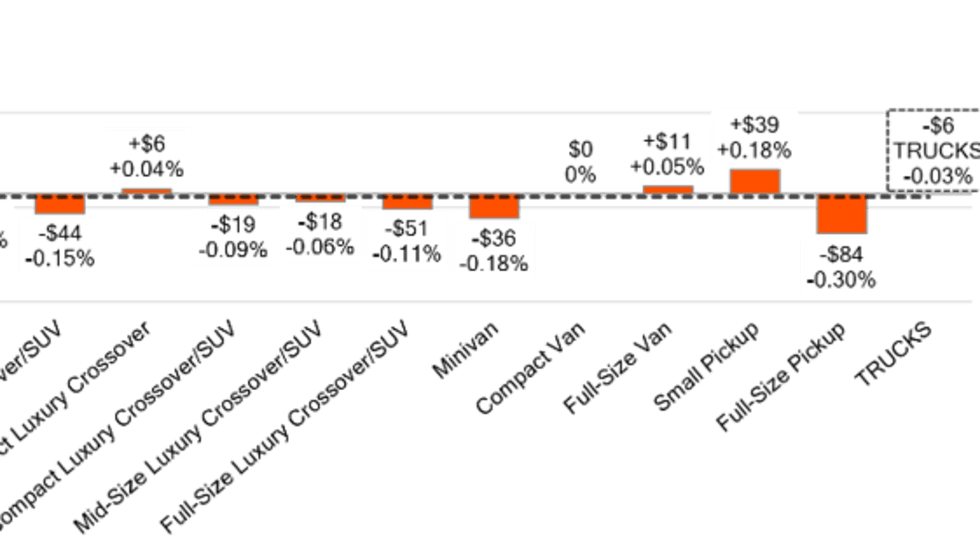

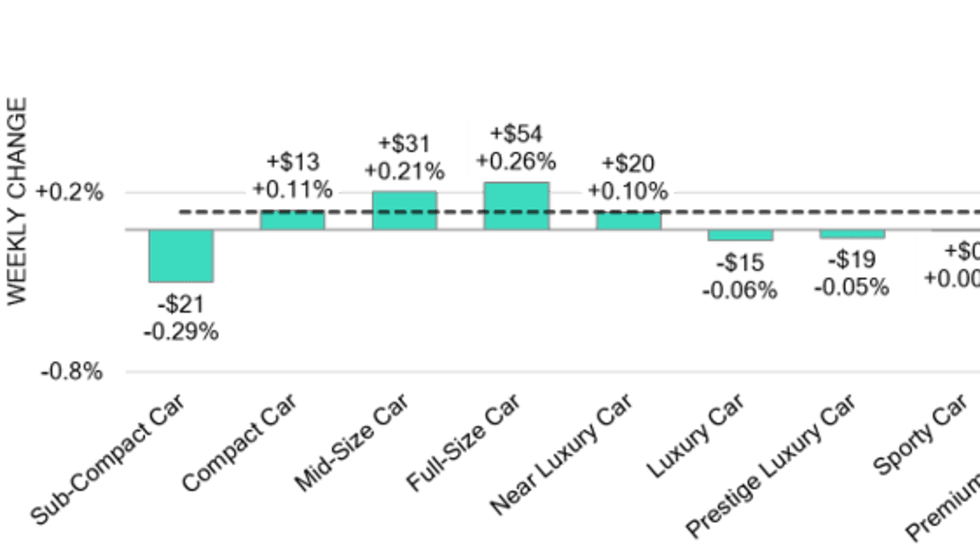

Black Book: Weekly Market Update

Wholesale values fell last week despite the spring season still being in the traditional full-gear mode, analysts said.

Read More →

Arkansas Auto Group Acquires First Indiana Rooftop

Performance Brokerage Services represented both the buyer and seller in the sale of Carver Toyota of Columbus by Carlock Automotive Group.

Read More →

Stellantis to Dive Into U.S. Lending

The multinational maker of Chrysler, Dodge, Jeep, Ram and multiple other brands received conditional approvals for a Utah-based industrial bank.

Read More →

New-Vehicle Prices Rise

With April sales down, higher prices on in-demand large vehicles helped inflate the overall ATP, though increases were under long-term averages, Cox Automotive reported.

Read More →

Black Book: Weekly Market Update

Last week in the wholesale automotive market proved to be a mixed bag, analysts reported.

Read More →

Black Book: Weekly Market Update

Conversion rates were flat last week at 63%, Black Book analysts calculated, as low-mileage and almost-near units outpaced the overall market.

Read More →

EU Auto Association Urges Action

Trade relations between the European Union and the U.S. are at risk, causing the European Automobile Manufacturers Association to push lawmakers to make a decision.

Read More →

Driving into the Super CFC Era

Understanding the risks and benefits of retail accounting and Super CFCs can help you better present options to your dealer partners.

Read More →