Wholesale vehicle prices moved up last week, and auction activity proved healthy, Black Book analysts observed. Get their complete market results here.

Black Book: Weekly Market Update

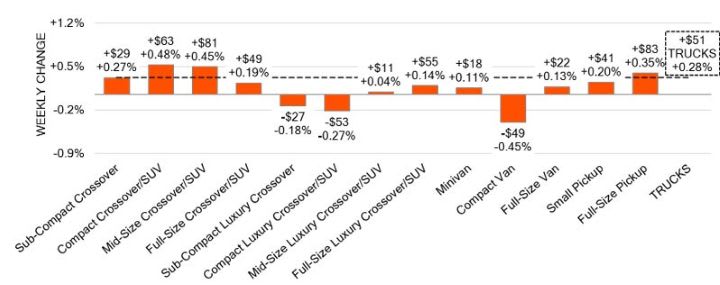

Conversions picked up last week at wholesale vehicle auctions, according to the market observer, as the spring shopping season appeared to begin.

March 3, 2026

Black Book

1 min to read

More Industry

Automakers Have More Tricks Up Their Sleeves

JD Power analysts see auto retail faring this year’s storms well through various means, though it acknowledges conditions are challenging to accurately predict.

Read More →

Insurance Rates Continue to Fall

Car insurance premiums have continued to decline so far this year, the overall national average settling at $138 per month in March, according to Insurify data.

Read More →

Black Book: Weekly Market Update

Last week's wholesale auction activity was stable, though buyers exercised selectivity as they focused on certain segments.

Read More →

Dealer Debrief: Safety, Supply & Partnership

In this week's Dealer Debrief, host Lauren Lawrence covers a new safety assessment, current inventory issues, and a new payables process for dealerships.

Read More →

Black Book: Weekly Market Update

Both conversions and values were up last week, though business was spotty depending on the segment in question.

Read More →

Stellantis Expands Charging Network

Five of its brands now have greater access to battery-electric vehicle charging through Tesla’s Supercharger network across North America.

Read More →

Safety Drives Insurance Rates

Sixteen out of the 20 cheapest vehicles to insure in 2026 are SUVs, according to CarInsurance.com, largely because of their safety features and lower repair costs.

Read More →

New-Vehicle Shoppers Get Some Relief

Overall conditions in February tipped slightly in consumers’ favor as prices stayed high, granting a reprieve of sorts just before the war on Iran commenced and started to reverse the welcome trend.

Read More →

Used Market Gains Speed

New-vehicle sales fell year-over-year for the fifth month in a row in February, making retail deliveries the slowest they’ve been since 2023, according to a CarGurus report.

Read More →

Auto Loan Defaults Measured Amid Inflation

According to LendingTree data, the average monthly auto loan payment was $540 in the fourth quarter, and the average credit score for those with a recorded default was 529.

Read More →