BLACK BOOK – Wholesale Prices, Week Ending November 6th

We have now had ten consecutive weeks of wholesale value increases, during a time that traditionally experiences large week-over-week declines. Limited inventory continues to be the driver of the market strength, particularly on vehicles that are desired by rental companies. The larger independent dealers are no longer the ones fueling the price increases, but instead it is the rental companies that need used vehicles to supplement their inability to get new inventory for their fleets.

This Week Last Week 2017-2019 Average (Same Week)

Car segments +0.83% +0.67% -0.79%

Truck & SUV segments +0.56% +0.66% -0.60%

Market +0.65% +0.66% -0.67%

Car Segments

On a volume-weighted basis, the overall Car segment increased +0.83%. For reference, the previous week, cars increased by +0.67%.

All nine car segments reported gains again last week.

Compact Cars (+1.45%) increased for the twelfth week in a row for an average weekly increase of +0.75%. Three of the last five weeks of increases exceeded 1% for Compacts.

Mid-Size Cars (+0.95%) also increased for the twelfth week in a row, but at a slower rate than the week prior (+1.08%).

Truck / SUV Segments

The volume-weighted, overall Truck segment increased +0.56%, compared to the prior week’s increase of +0.66%.

All thirteen truck segments reported gains last week.

Compact (+1.03%), Sub-Compact Luxury (+1.10%), and Compact Luxury (+1.15%) Crossovers all reported gains exceeding 1%.

Full-Size Vans (+1.02%) also reported a gain exceeding 1%. The segment has now had increases for forty out of the last forty-one weeks.

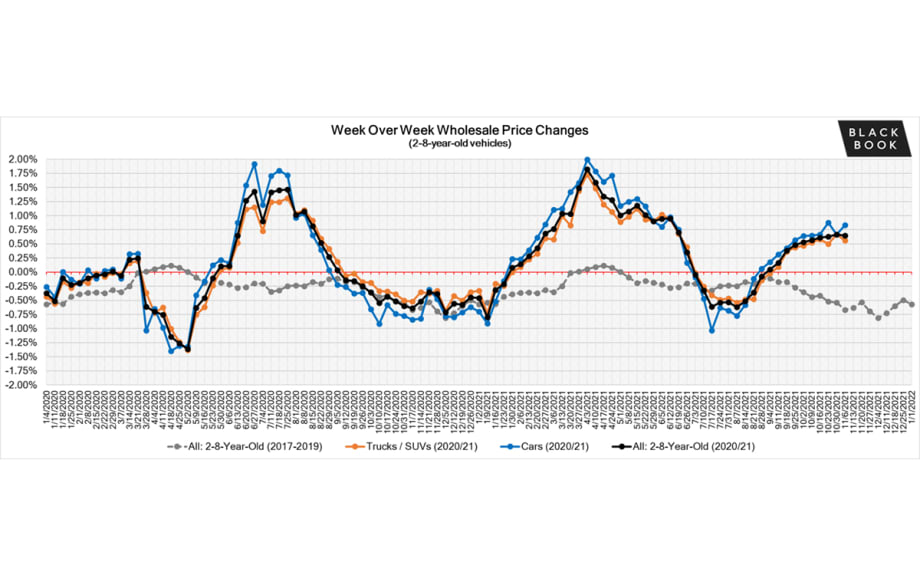

Weekly Wholesale Index

Calendar year 2020 ended with used wholesale prices at elevated levels. With economic patterns (including the automotive market) driven by the pandemic, normal seasonal patterns (e.g., 2019 calendar year) in the wholesale market were not observed for most of the year. We saw a similar picture in 2009, at the end of the Great Recession. Calendar year 2021 has not had typical seasonality patterns as the market has had rapid increases in wholesale values for the majority of the year. After reaching record heights at the end of June, wholesale prices began to decline at a rate higher than the typical seasonal decline through July and most of August. As we moved into the Fall season, wholesale prices began to show a positive movement once again and reached the highest point of the year last week again, at 1.46.

The graph below looks at trends in wholesale prices of 2-6-year-old vehicles, indexed to the first week of the year.

Retail (Used and New) Insights

As the brand prepares for an all-electric vehicle lineup, Cadillac has restructured their US dealer network and expects to have 560 dealerships by the end of year, compared to over 900 dealers 3 years ago, with a hefty buy out price tag of $274M.

Production of the 2022 Chevrolet Bolt EV and Bolt EUV is back on temporarily, as GM continues to work through a large-scale battery recall. The Orion Assembly plant in Michigan is scheduled to stop production for 3 weeks in mid-November.

The U.S. House of Representatives passed a $1.2T bipartisan infrastructure bill that designates $65B for upgrades of the nation’s electric grid and $7.5B for the nationwide deployment of EV charging stations, which could triple the number of charging stations.

Hertz recently announced a $4.2B order for 100,000 vehicles from Tesla to add to its rental fleet by the end of 2022.

The Volkswagen Group of America is partnering with the U.S. DOE in joint research on wireless charging; they aim to charge the Porsche Taycan to 80% in 10 minutes, without bulky charge cords.

Used Retail Prices

With the proliferation of ‘no-haggle pricing’ for used-vehicle retailing, asking prices accurately measure trends in the retail space. Retail demand slowed down at the end of last year, and thus resulted in declining retail asking prices for the last several weeks of 2020. As demand rebounded, retail prices have lagged slightly behind wholesale prices, but March had an accelerated growth in retail prices. In April and May, retail prices picked up speed as demand accelerated, fueled by stimulus payments, tax season, and shortages of new inventory. During the third quarter, retail prices continued to rise at a slower rate but have since picked up. After continued strong increases, the retail listing prices index has increased to just over 31% above where we started the year.

This analysis is based on approximately two million vehicles listed for sale on US dealer lots. The graph below looks at 2-6-year-old vehicles.

Inventory

Used Retail

Typically, used inventory significantly increases in Q4 as manufacturers and dealers switch over to the new model year. This year, due to the microchip shortage, we do not expect such a high volume of used vehicles. In the last four weeks, used inventory stopped declining and stabilized at around 16% below where we started the year.

Days-to-turn for used retail listings decreased over the last month, after a few weeks of slight increases. The days-to-turn now sits just above 36 days, which is lower than what is typically expected in a normal year.

Wholesale

As fuel prices continue to rise, smaller vehicles seem to be outperforming their larger counterparts. As we get down to the last months of the year, large independent dealers and franchise dealers have picked up in presence. Rental companies still seem to be dominating the physical lanes, especially when newer, low mile vehicles are offered. While new inventory is slowly seeping into the market, it is at much lower levels than typically expected at this point in the year, so the wholesale lanes continue to be a main source of inventory even though wholesale prices on some vehicles have soared past the manufacturer suggested MSRP.

The overall wholesale market for 2-8-year-old vehicles increased by +0.65% last week, and 0-2-year-old vehicles increased +0.70%.