Black Book Market Insights – 10/25/2022

Wholesale Prices, Week Ending October 22nd

The market is continuing to experience larger than typical declines for the time of year. However, the older vehicles, those aged 8-to-16 years old, are not depreciating as fast; last week, 8-to-16-year-old vehicles depreciated -0.63%, compared with the 2-to-8-year-old vehicles that depreciated -0.76%.

This Week Last Week 2017-2019 Average (Same Week)

Car segments -0.89% -1.11% -0.57%

Truck & SUV segments -0.70% -0.67% -0.48%

Market -0.76% -0.82% -0.52%

Car Segments

On a volume-weighted basis, the overall Car segment decreased -0.89%. For reference, the previous week, cars decreased by -1.11%.

All nine Car segments decreased last week.

Three segments reported declines greater than 1% last week: Compact Car (-1.01%), Near Luxury Car (-1.11%), and Prestige Luxury Car (-1.23%). All three of these segments also had declines exceeding 1% the week prior.

Premium Sporty Car depreciation has slowed in recent weeks, for an average weekly depreciation over the last three weeks of -0.36%.

Truck / SUV Segments

The volume-weighted, overall Truck segment decreased -0.70%, which is consistent with the prior week’s decrease of -0.67%.

All thirteen truck segments reported declines.

Compact (-0.22%) and Full-Size (-0.25%) Van continue to decline, but are reporting the smallest declines across all of the segments.

Compact Crossovers (-0.82%) have remained consistent with the rate of decline over the last 6 weeks, with an average weekly decline of -0.86%.

Weekly Wholesale Index

Calendar year 2020 and 2021 ended with used wholesale prices at elevated levels. With economic patterns (including the automotive market) driven by the pandemic, normal seasonal patterns (e.g., 2019 calendar year) in the wholesale market were not observed for most of the last 2 years. We saw a similar picture in 2009, at the end of the Great Recession. Calendar year 2021 did not have typical seasonality patterns as the market had rapid increases in wholesale values for the majority of the year. The Wholesale Weekly Price Index reached the highest point of the year at the end of December 2021, reporting over 1.51 points.

The graph below looks at trends in wholesale prices of 2-6-year-old vehicles, indexed to the first week of the year. The index is computed keeping the average age of the mix constant to identify market movements.

Retail (Used and New) Insights

GMC recently introduced the Sierra EV Denali, which is expected to have up to 400 miles of range and 754 hp. 2 more EV models – the Elevation and the AT4 – are expected before 2025.

BMW announced a $1.7B investment in their South Carolina facility over the next 8 years to build new battery-powered vehicles.

Stellantis is looking to add 2 more EV-battery plants in North America before 2030, in addition to their plants in Indiana and Canada.

Foxconn Technology Group unveiled their all-electric Model B crossover and Model V pickup truck. The company previously purchased Lordstown Motors Corp.’s Ohio plant.

The U.S. federal administration awarded $2.8B in grants to 20 companies across at least 12 states to increase manufacturing EV batteries and mineral production in the U.S.

In Europe, Jeep unveiled their first EV model – the Avenger – at the Paris Motor Show. Smaller than the Compass and Renegade, the Avenger has been dubbed a “pocket-sized EV” and will not be available stateside.

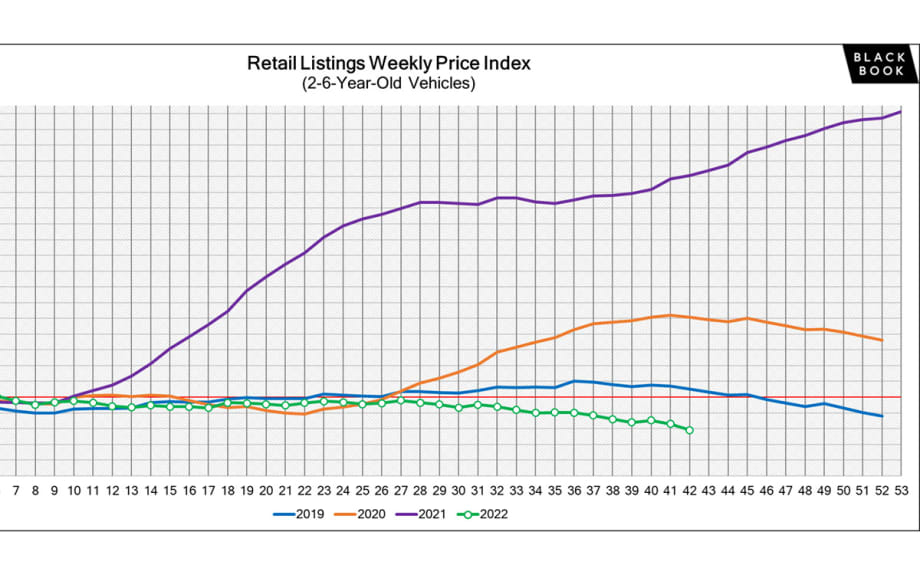

Used Retail Prices

Used Retail Prices are more accessible than in years past, due to the proliferation of ‘no-haggle pricing’ for used-vehicle retailing. Transparent pricing upfront makes the car buying process more enjoyable for customers and allows Black Book to accurately measure retail market trends.

At the on-set of the pandemic, in CY2020, used retail prices increased slightly, following typical seasonal patterns, and then began dropping in April, finally hitting a low point in the late spring months. By late summer of CY2020, Used Retail Prices increased as supply of new vehicle inventory started to become scarce, but retail demand slowed down at the end of CY2020, resulting in declining retail asking prices for the last several weeks of the year. When CY2021 kicked off, demand rebounded while retail prices lagged slightly behind wholesale prices; March of 2021 started the dramatic increases in Used Retail Prices, fueled by stimulus payments, tax season, and shortages of new inventory. During the third quarter, retail prices continued to rise at a slower rate but soon picked up the pace once again to start the fourth quarter. In Q4, prices on retail listings steadily increased week after week. As CY2021 came to an end, the retail listing price index closed 36% above where the year began.

Now, in the fourth quarter of 2022, the Retail Listings Price Index has started to decline, but not as steep as the wholesale price index.

This analysis is based on approximately two million vehicles listed for sale on U.S. dealer lots. The graph below looks at 2-6-year-old vehicles. The Index is computed keeping the average age of the mix constant to identify market movements.

Inventory

Used Retail

Used retail active listing volume remained around 1.13 for the third consecutive week.

The Used Retail Days-to-Turn Estimate is around 45 days.

Wholesale

Inventory was up last week, which could be a good sign of sellers softening their floors. There were some If sales that trickled in which is also a good sign that sellers are more willing to negotiate with the buyers. Buyer count was stable the last couple of weeks, which could mean they are holding firm and trying to negotiate with the sellers. Sales rates were better in certain lanes, but overall, they decreased compared to prior weeks. There are still not a lot of buyers physically in the lanes, but that is not stopping them from bidding online. Franchise dealers took advantage of the absence of the independent large dealers and dominated in the lanes. Rental companies occasionally would show up and compete, but they were not as consistent as the franchise dealers. There are still very few Model Year 2023 vehicles coming through, but we expect to see more as we close out the year and see more launches of 2024 vehicles. Overall, it seemed to be a stable week in the wholesale market.

The Estimated Average Weekly Sales Rate dropped to 54% last week.