Considerations When Designing New Products: An Update

Considerations When Designing New Products: An Update

Working in the F&I industry stays interesting because of the great products that our industry continues to develop to meet the needs of the public. In 2011, we wrote a short article on developing new products. Since that time, the amount and complexity of new products in the F&I space has only increased.

In developing a new product, there are, of course, many issues regarding such concerns as policy language, pricing, marketing, and systems. We want to focus on some general considerations when developing a product from a pricing and accounting standpoint. Let’s tackle the subject in FAQ format.

Do I Have Any Claims Experience?

Obviously, if you have related claims experience, it can be of tremendous help in determining the potential exposure for your product. Industry experience can be helpful. Census data, crime statistics, and data designed for the auto industry can help solidify assumptions.

How Is the Product Marketed?

Similar products can have vastly different claims experiences depending on how they are marketed. Will the product be marketed to new buyers or to current owners? Is the product marketed at the dealership or direct marketed? What is your expected pricing?

The amount of money that a consumer pays can impact claims consciousness as well. A low-price product will have lower awareness.

Embedded products, which are part of the sale of every applicable item and not charged separately, are increasingly popular. These products typically will have a much lower claims rate. This may be due to consumer’s forgetting about the benefit since they didn’t explicitly pay for it.

A great example of this is that many credit cards include protection for items bought within a certain period. Have you ever made a claim for an item bought on a credit card? Do you think you could have?

How Am I Going to Earn the Premium?

This is a critical assumption for evaluating early experience. Claims occur on F&I products at vastly different rates depending on the product. Some products (even profitable ones) have an initial surge of claims as the buyer may seek to repair some preexisting issues that cannot be fully excluded. Never assume that exclusions can prevent all claims.

To evaluate the experience correctly, you must earn the premium in the same ratio as the claims flow. You may need to earn premium differently for accounting and refunding than you do to evaluate the program. While earnings are necessarily subjective, be careful to use your best estimate.

Some programs, such as lease wear-and-tear, will have virtually no claims experience until the contract is at, or near, the end. You may want to make more careful assumptions about these products because once you see the results you may have a large amount of unearned exposure.

How Will I React to the Results?

Everyone who develops a product expects it to succeed. Don’t let your prior assumptions blind you to the results in your book!

Most F&I products are relatively high-frequency/low-severity products that reach credibility in a short amount of time. If you are earning your exposures correctly (see above), your results could be actionable in a few months. Plan on frequent monitoring after the product launch to ensure that the program is performing to your expectations.

Divide the experience into months or quarters by policy inception date and examine the experience of the most mature contracts carefully. For example, if you expected a “claims surge” for the first few months after the sale of a product, are you seeing the claims from your oldest contracts dropping? If not, you may need to reevaluate your assumptions.

If an Insured Makes a Claim, Will They Be in a Better Financial Position?

Most insurance products operate on the premise that the insured will not be better off financially after a claim. For example, auto insurance will pay the actual cash value of your car. In theory, you could go out and buy the same model car with similar mileage. You cannot buy a brand-new car.

Some products, such as GAP insurance, improve the customer’s financial situation. If you have a GAP claim, the negative equity in your vehicle is erased. A similar example occurs in homeowner’s insurance, which typically offers “replacement value” for your house and contents. If a fire destroys your house, you will receive new furniture and clothes — not the old stuff you had.

These insurance products work because the vast majority of people do not wish to have a fire or a car wreck, even if it improves their personal balance sheet slightly. However, you can expect that these types of products will have higher claims because there are always a few people who will use the product to their advantage.

Will the Claims Be Correlated With the Economy?

For most products, this is not true. Unexpected repairs and collisions are examples of random events. While certain people and certain vehicles may be more likely to have a claim, in general, the claims among similar risks are random.

However, this is not true for all products. Some products will show a higher propensity of claims due to the economic environment. This type of risk can occur when insuring the underlying value of an asset, such as with GAP or residual value insurance. If the used car market shows a big drop in prices, the likelihood and severity of claims will increase across the board. If your product is correlated with the economic environment, be prepared for a wide range of results depending on the conditions of our economy.

New products are what make the F&I business one of the most exciting places in insurance for product development. While the considerations listed above may give you pause, we encourage our industry to continue to develop products which meet the needs of all participants, by providing peace of mind to the buyer and an adequate return to the underwriter and business partners.

More Actuary

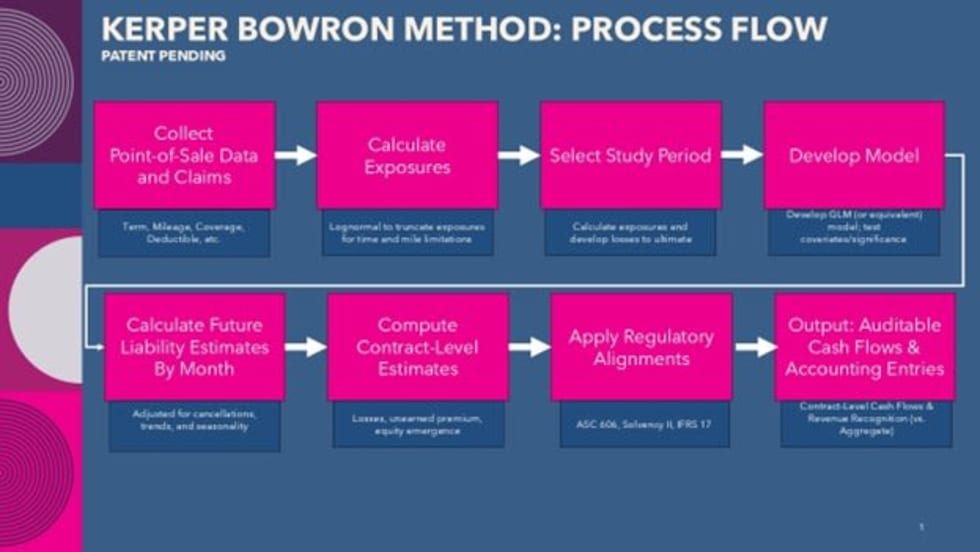

The Future of Service Contract Accounting

The Kerper Bowron Method is a patent-pending approach that builds on established actuarial principles but applies them at the individual contract level.

Read More →

Tougher Standards Mean Fewer IIHS Safety Awards

Fewer vehicles earned the honor in 2023 than last year as group toughens safety evaluation standards.

Read More →

Kelley Blue Book Names 2021 Best Resale Value Award Winners

An average 2021 model-year vehicle will only retain about 40% of its original value after a five-year ownership period.

Read More →

Autotrader Names 10 Best Car Interiors Under $50,000 for 2020

To help car buyers look beyond a new car’s outward appearance and focus more on the beauty within, the experts at Autotrader recently named the 10 Best Car Interiors Under $50,000 for 2020.

Read More →

Will ASC 606 Impact Me?

Released in 2014 and in effect private companies as of this year, the FASB’s ASC 606 will have a significant impact on the P&A segment. Actuarial experts break down the new standard and answer your FAQs.

Read More →

Spireon Wins IoT Breakthrough Award

Spireon’s GoldStar GPS solution earned the company Connected Car Product of the Year honors in the 2019 IoT Breakthrough Awards.

Read More →

Ziegler: They Said I Was a Crackpot

Jim Ziegler holds Uber responsible for the death of an Arizona woman who was run down by an autonomous SUV in March, but he doubts executives will face criminal charges. In They Finally Killed Somebody , the Alpha Dawg traces the so-called demand for driverless vehicles to the handful of businesses that stand to gain the most — including some of your closest partners. Click here to read the story.

Read More →

Ziegler to GMs: Don’t Sell Yourself Short

If you are an executive general manager making $500,000 a year, this video is not for you. If not, listen up, because Jim Ziegler is here to help. In an exclusive to Auto Dealer Today , the Alpha Dawg lists the 20 Things a GM Must Do Every Week to become an executive GM, take your dealership to new heights, and maximize your personal income. Click here to read the story.

Read More →