Released in 2014 and in effect private companies as of this year, the FASB’s ASC 606 will have a significant impact on the P&A segment. Actuarial experts break down the new standard and answer your FAQs.

by Lee Bowron and John Kerper

October 31, 2019

Released in 2014 and in effect private companies as of this year, the FASB’s ASC 606 will have a significant impact on the P&A segment. Actuarial experts break down the new standard and answer your FAQs.

Photo by Sean Gladwell via GettyImages

4 min to read

The Financial Accounting Standards Board’s ASC 606 will have a major accounting impact for any entity which receives contingent commissions, or “retros.” In general, you will be required to recognize any estimated future commissions or retrospective payments as revenue at contract inception.

It may also apply if you have an excess contractual liability policy and place the funds in a trust account in which the trust account is not part of the assets of an insurance company.

Ad Loading...

For private companies, “Accounting Standards Update 2014-09: Revenue from Contracts with Customers and created Accounting Standards Codification Section 606” (as it is formally known) is effective for annual reporting periods beginning this year.

For example, suppose you have a retroactive commission for a block of service contracts. The commission is defined as 100% and loss ratio as 10%. Therefore, the insurance company is allowed a 10% margin before paying commissions. Typically, deals such as these have formulas on paying these commissions, such as the book must be 50% earned.

The actual accounting standard relates to a five-part accounting test:

Part 1: Identify the contract. This part is easy; it is just the service contract.

Ad Loading...

Part 2: Identify the separate performance obligations within a contract. Typically, the performance obligations would be paying claims, issuing refunds, and perhaps claim adjustment expenses. When these occur, they will generally not be uniform over the life of the contract.

Part 3: Determine the transaction price.

Part 4: Allocate the transaction price to the performance obligations.

Part 5: Recognize revenue as each performance obligation is realized. This would typically be done using an earnings curve to recognize revenue in proportion to losses.

With all that in mind, let’s address a few frequently asked questions:

Ad Loading...

WHOM DOES THIS IMPACT?

ACS 606 will impact any entity reporting under GAAP accounting standards, which is not an insurance company. For example, if you are an administrator and have a contractual liability reimbursement policy, the underlying loss experience might be reinsured into a controlled reinsurance company. This would be exempt.

However, if you receive a retrospective commission or hold the funds under an excess contractual liability policy, you would likely be subject to this guidance.

WHEN IS THIS EFFECTIVE, AND WHAT ABOUT MY EXISTING CONTRACTS?

For private companies, this standard is effective for annual reporting periods after Dec. 15, 2018. Therefore, if your fiscal year-end is Dec. 31, 2019, it would be effective

Ad Loading...

for this annual reporting period. There are transition rules which provide different options for contracts which originated under the prior standard.

WHY IS THIS HAPPENING AND HOW IS THIS DIFFERENT?

Under U.S. GAAP accounting standards, revenue recognition was often complex and there were different rules for different industries. ASC 606 is more “inline” with international standards and provides a principles-based approach for revenue recognition across various industries.

In the past, most companies simply recognized this type of contingent revenue when received.

CAN YOU GIVE ME AN EXAMPLE?

Ad Loading...

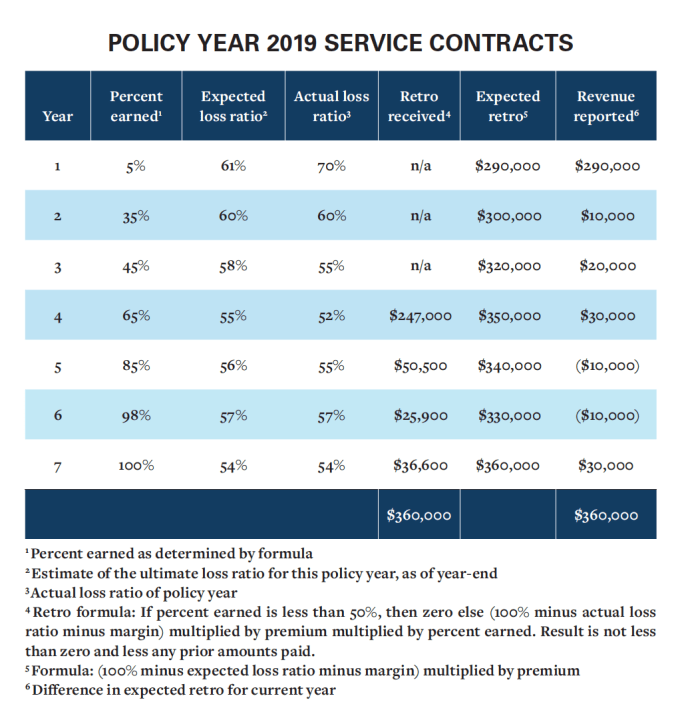

The table below is a hypothetical example of revenue recognition under ASC 606 compared to actual received payments, assuming a premium of $100,000, a 10% margin, a retro of 100% minus loss ratio minus margin paid when 50% is earned, and an initial expected loss ratio of 60%:

In this example, most of the revenue is received in Year Four, but the entire estimated retro is recognized in Year One. The revenue in future years simply reflects a “true-up” between the initial estimate and the revised estimate and actual results. Actual receipt of contingent revenue does not impact the revenue reported. After all contracts have expired, the total revenue recognized and received is the same.

Audited GAAP financial statements will need support on assumptions regarding retrospective revenue. As a practical matter, revenue will increase for the first few years until prior contracts have expired.

Since insurance entities are exempt from these requirements, it may make reinsurance or other risk transfer mechanisms more favorable.

And, of course, any individual situation will be fact dependent and you should rely on your accountant and actuary for appropriate advice on your situation.

Ad Loading...

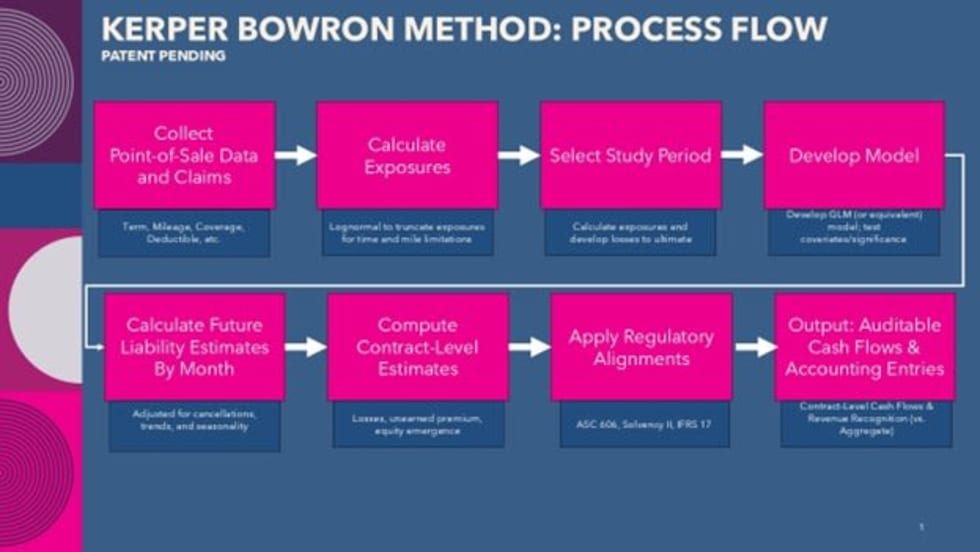

LEE BOWRON, ACAS, MAAA AND JOHN KERPER, FSA, MAAA ARE CO-FOUNDERS OF ACTUARIAL AND INSURANCE CONSULTING FIRM KERPER AND BOWRON LLC.

The Kerper Bowron Method is a patent-pending approach that builds on established actuarial principles but applies them at the individual contract level.

To help car buyers look beyond a new car’s outward appearance and focus more on the beauty within, the experts at Autotrader recently named the 10 Best Car Interiors Under $50,000 for 2020.

Released in 2014 and in effect private companies as of this year, the FASB’s ASC 606 will have a significant impact on the P&A segment. Actuarial experts break down the new standard and answer your FAQs.

Jim Ziegler holds Uber responsible for the death of an Arizona woman who was run down by an autonomous SUV in March, but he doubts executives will face criminal charges. In They Finally Killed Somebody , the Alpha Dawg traces the so-called demand for driverless vehicles to the handful of businesses that stand to gain the most — including some of your closest partners. Click here to read the story.

If you are an executive general manager making $500,000 a year, this video is not for you. If not, listen up, because Jim Ziegler is here to help. In an exclusive to Auto Dealer Today , the Alpha Dawg lists the 20 Things a GM Must Do Every Week to become an executive GM, take your dealership to new heights, and maximize your personal income. Click here to read the story.